Ninepoint Global Real Estate Fund

January 2024 Commentary

Summary

- Ninepoint Global Real Estate Fund had a YTD return of -1.30% up to January 31, compared to the MSCI World IMI Core Real Estate Index with a total return of -2.60%.

- The Communication and Information Technology sectors continued their upward trend into 2024, while Real Estate and Utilities sectors lagged due to a slight increase in US 10-year Treasury bond yields.

- The Federal Reserve held interest rates steady at 5.25% to 5.50% during the January FOMC meeting, maintaining a tough stance to prevent inflation resurgence, with no significant change in policy direction indicated for the near term.

- Expectations for the initial rate cut have shifted to May or June of 2024, with the anticipation of some market volatility in the first half of the year as investors await clearer signs of monetary policy easing.

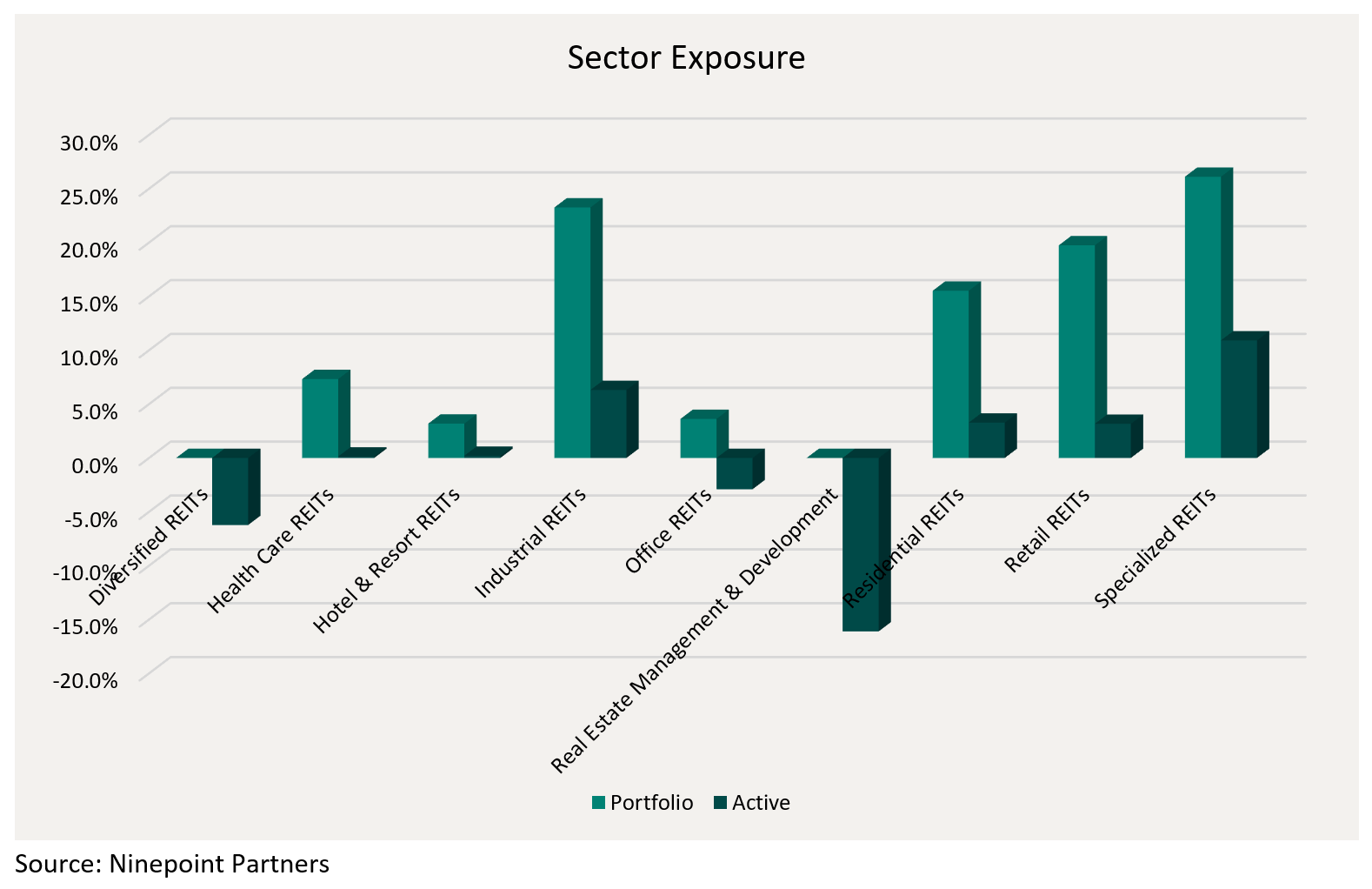

- The Fund is currently overweight Specialized REITs, Industrial REITs, and Residential REITs while underweight Real Estate Management & Development, Diversified REITs, and Office REITs.

- The fund was concentrated in 28 positions, with the top 10 holdings accounting for approximately 43.3% of the fund. Over the prior fiscal year, 18 out of our 28 holdings have announced a dividend increase, with an average hike of 14.7% (median hike of 3.3%).

Monthly Update

Year-to-date to January 31, the Ninepoint Global Real Estate Fund generated a total return of -1.30% compared to the MSCI World IMI Core Real Estate Index, which generated a total return of -2.60%.

Ninepoint Global Real Estate Fund - Compounded Returns¹ As of January 31, 2024 (Series F NPP132) | Inception Date: August 5, 2015

| 1M | YTD | 3M | 6M | 1YR | 3YR | 5YR | Inception | |

| Fund | -1.3% | -1.3% | 12.0% | 0.4% | -6.1% | 2.6% | 3.8% | 5.9% |

| MSCI World IMI Core Real Estate NR (CAD) | -2.6% | -2.6% | 12.3% | 2.7% | -2.3% | 1.8% | 0.8% | 2.7% |

The year 2024 has started off much like 2023 ended, with stocks in the Communication and Information Technology sectors continuing to rally. However, after peaking last October and falling through the end of the year, the US 10-year Treasury bond yield retraced some of its recent move lower this past month. As rates ticked slightly higher in January, rate-sensitive securities in the Real Estate and Utilities sectors underperformed. Longer term, we are not overly concerned about this backup in rates, since we believe that those looking for immediate rate cuts simply got ahead of themselves towards the end of last year. Instead of focusing on the near term, investors should take a step back and focus on the bigger picture: inflation is easing, growth remains resilient, the jobs market remains strong, the earnings recession is over and rate cuts will begin sometime in 2024.

At the January FOMC meeting, the Fed unsurprisingly held rates steady at a range of 5.25% to 5.50%. As we’ve discussed previously, we’ve been reasonably confident that the final interest rate hike for the cycle occurred at the July meeting, but we recognized that Fed officials would continue to talk tough to prevent resurgent inflation. During Powell’s press conference on January 31, the Chairman stuck to this script, saying “So if you take that to the current context, we’re going to be data dependent. We’re going to be looking at this meeting by meeting. Based on the meeting today, I would tell you that I don’t think it’s likely that the Committee will reach a level of confidence [to cut rates] by the time of the March meeting, to identify March as the time to do that. But that’s to be seen”. We don’t see anything in that statement that changes our view that the Fed is taking a more balanced view in pursuit of their dual mandate of full employment and price stability.

Admittedly, the odds of a March cut are lower today (but not zero) and the most likely scenarios suggest an initial rate cut in May or June of 2024. After almost two years since the first interest rate hike, we accept the need to wait patiently for another two or three months before an easier monetary policy. But because the precise timing is unknown and the future economic environment remains uncertain, it would be reasonable to expect some volatility in the first half of 2024. Further, with the S&P 500 currently above 4,900 (or almost 20x 2024 forward earnings according to FactSet), it feels like investors have optimistically pulled forward some future returns. Therefore, after a flat year of earnings growth in 2023, a return to earnings growth in 2024 (currently forecasted at just under 10%, again according to FactSet) will be required for the market to continue to move significantly higher over the balance of the year.

Nevertheless, if growth does meet expectations and mega-cap tech moves sideways or even underperforms in 2024 from here (quite possible given the high expectations and high multiples already applied to these equities), our dividend focused mandates should do well on both an absolute and relative basis. As always, we are continually searching for companies that are expected to post solid revenue, earnings and dividend growth but still trade at acceptable valuations today.

For the Ninepoint Global Real Estate Fund, we are concentrating our research efforts on high quality, dividend growth companies given our positive assessment of the risk/reward outlook over the next few years. After many years of outperformance from the high growth and high valuation Information Technology sector, if interest rates fall and earnings and cash flow growth become more widespread, we would expect a rotation out of the big winners of 2023 and into undervalued equities and REITs more aligned with our dividend-focused mandates in 2024.

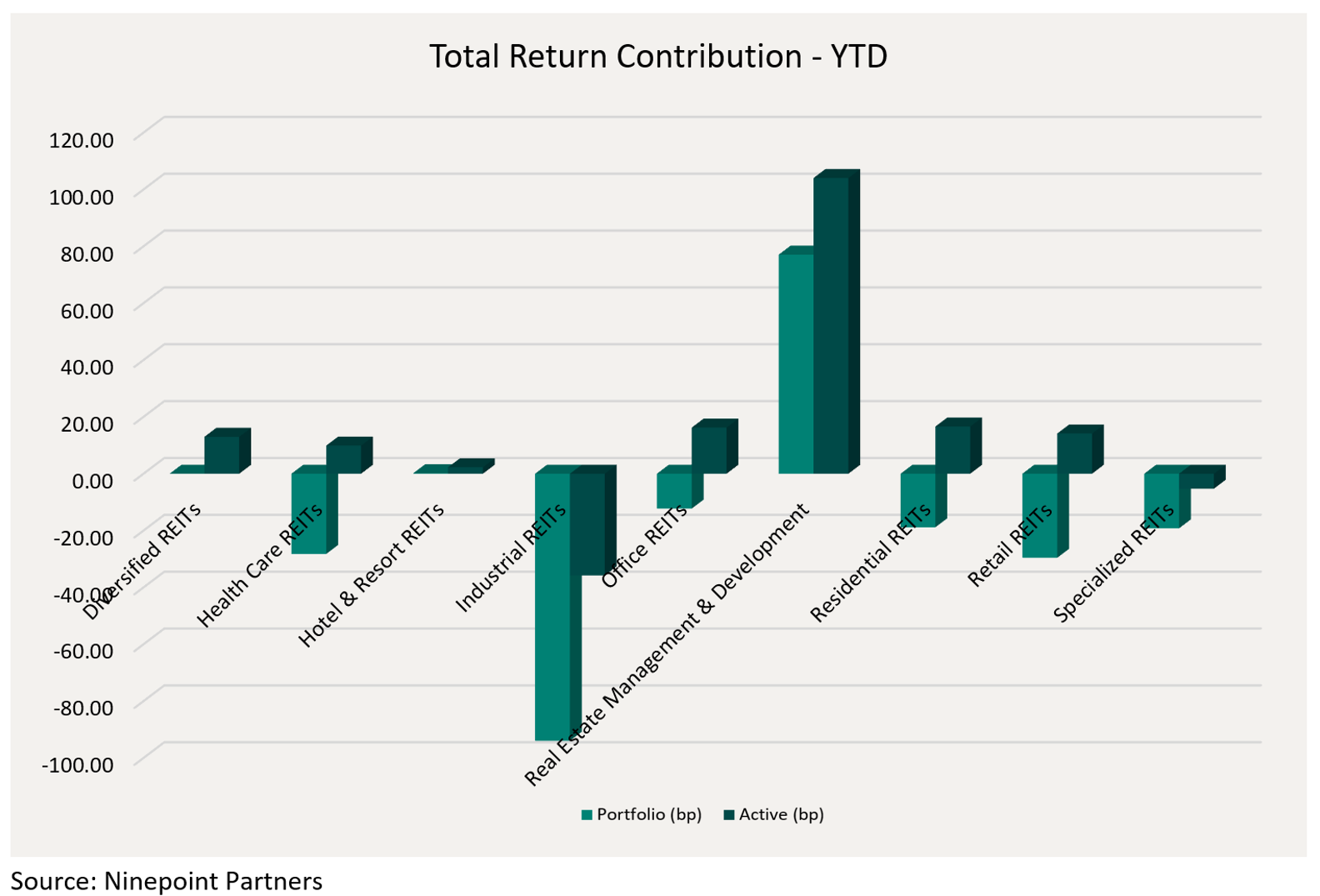

Top contributors to the year-to-date performance of the Ninepoint Global Real Estate Fund by Industry included Real |Estate Management & Development (+77 bps) and Hotel & Resort REITs (+1 bps), while top detractors by sub-industry included Industrial REITs (-94 bps), Retail REITs (-30 bps) and Health Care REITs (-28 bps) on an absolute basis.

On a relative basis, positive return contributions from the Real Estate Management & Development (+104 bps), Residential REITs (+16 bps) and Office REITs (+16 bps) industries were offset by negative contributions from the Industrial REITs (-36 bps) and Specialized REITs (-5 bps) industries.

We are currently overweight Specialized REITs, Industrial REITs, and Residential REITs while underweight Real Estate Management & Development, Diversified REITs, and Office REITs. With the debate shifting toward the timing of the first interest rate cut of the cycle, we are looking forward to better relative performance from dividend paying real estate assets in 2024. In the meantime, we remain focused on high quality, dividend payers that have demonstrated the ability to consistently generate revenue and cash flow growth through the business cycle.

The Ninepoint Global Real Estate Fund was concentrated in 28 positions as at January 31, 2024 with the top 10 holdings accounting for approximately 43.3% of the fund. Over the prior fiscal year, 18 out of our 28 holdings have announced a dividend increase, with an average hike of 14.7% (median hike of 3.3%). Using a total real estate approach, we will continue to apply a disciplined investment process, balancing valuation, growth, and yield in an effort to generate solid risk-adjusted returns.

Jeffrey Sayer, CFA

Ninepoint Partners

Effective February 7, 2017 the Sprott Global REIT & Property Equity Fund’s name was changed to Sprott Global Real Estate Fund, subsequently on August 1, 2017 becoming Ninepoint Global Real Estate Fund.

1All returns and fund details are a) based on Series F units; b) net of fees; c) annualized if period is greater than one year; d) as at January 31, 2024; e) 2015 annual returns are from 08/04/15 to 12/31/15. The index is 100% MSCI World IMI Core Real Estate NR (CAD) and is computed by Ninepoint Partners LP based on publicly available index information.

The Fund is generally exposed to the following risks. See the Simplified Prospectus of the Fund for a description of these risks: capital depletion risk, concentration risk, credit risk, currency risk, cybersecurity risk; derivatives risk, emerging markets risk, equity real estate investment trust (REIT) risk, exchange traded funds risk, foreign investment risk, income trust risk, inflation risk, interest rate risk, liquidity risk, market risk, preferred stock risk; real estate risk; regulatory risk; securities lending, repurchase and reverse purchase transaction risk; series risk; short selling risk; specific issuer risk; substantial securityholfer risk; tax risk.

Ninepoint Partners LP is the investment manager to the Ninepoint Funds (collectively, the “Funds”). Commissions, trailing commissions, management fees, performance fees (if any), and other expenses all may be associated with investing in the Funds. Please read the prospectus carefully before investing. The indicated rate of return for series F units of the Fund for the period ended January 31, 2024 is based on the historical annual compounded total return including changes in unit value and reinvestment of all distributions and does not take into account sales, redemption, distribution or optional charges or income taxes payable by any unitholder that would have reduced returns. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated. The information contained herein does not constitute an offer or solicitation by anyone in the United States or in any other jurisdiction in which such an offer or solicitation is not authorized or to any person to whom it is unlawful to make such an offer or solicitation. Prospective investors who are not resident in Canada should contact their financial advisor to determine whether securities of the Fund may be lawfully sold in their jurisdiction.

The opinions, estimates and projections (“information”) contained within this report are solely those of Ninepoint Partners LP and are subject to change without notice. Ninepoint Partners makes every effort to ensure that the information has been derived from sources believed to be reliable and accurate. However, Ninepoint Partners assumes no responsibility for any losses or damages, whether direct or indirect, which arise out of the use of this information. Ninepoint Partners is not under any obligation to update or keep current the information contained herein. The information should not be regarded by recipients as a substitute for the exercise of their own judgment. Please contact your own personal advisor on your particular circumstances. Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any investment funds managed by Ninepoint Partners. Any reference to a particular company is for illustrative purposes only and should not to be considered as investment advice or a recommendation to buy or sell nor should it be considered as an indication of how the portfolio of any investment fund managed by Ninepoint Partners is or will be invested. Ninepoint Partners and/or its affiliates may collectively beneficially own/control 1% or more of any class of the equity securities of the issuers mentioned in this report. Ninepoint Partners and/or its affiliates may hold short position in any class of the equity securities of the issuers mentioned in this report. During the preceding 12 months, Ninepoint Partners and/or its affiliates may have received remuneration other than normal course investment advisory or trade execution services from the issuers mentioned in this report.

Ninepoint Partners LP: Toll Free: 1.866.299.9906. DEALER SERVICES: CIBC Mellon GSSC Record Keeping Services: Toll Free: 1.877.358.0540

Related Funds

1.3%

Historical Commentary

- Global Real Estate Fund 12/2023

- Global Real Estate Fund 11/2023

- Global Real Estate Fund 10/2023

- Global Real Estate Fund 09/2023

- Global Real Estate Fund 08/2023

- Global Real Estate Fund 07/2023

- Global Real Estate Fund 06/2023

- Jeff Sayer - H1 2023 Market Review and Outlook - Real Asset Strategies

- Global Real Estate Fund 05/2023

- Global Real Estate Fund 04/2023

- Global Real Estate Fund 03/2023

- Global Real Estate Fund 02/2023

- Global Real Estate Fund 01/2023

Toronto, Ontario M5J 2J1 Canada