Ninepoint Fixed Income Strategy

March 2024 Commentary

Monthly commentary discusses recent developments across the Ninepoint Diversified Bond, Ninepoint Alternative Credit Opportunities and Ninepoint Credit Income Opportunities Funds.

Summary

- North American Central Bankers are clearly advocating patience with interest rates.

- Stronger economic data (even in Canada) means there’s no rush to cut rates.

- Services inflation remains sticky, and higher energy prices could drive headline inflation back up.

- We remain defensively positioned until more interesting opportunities arise.

Economics

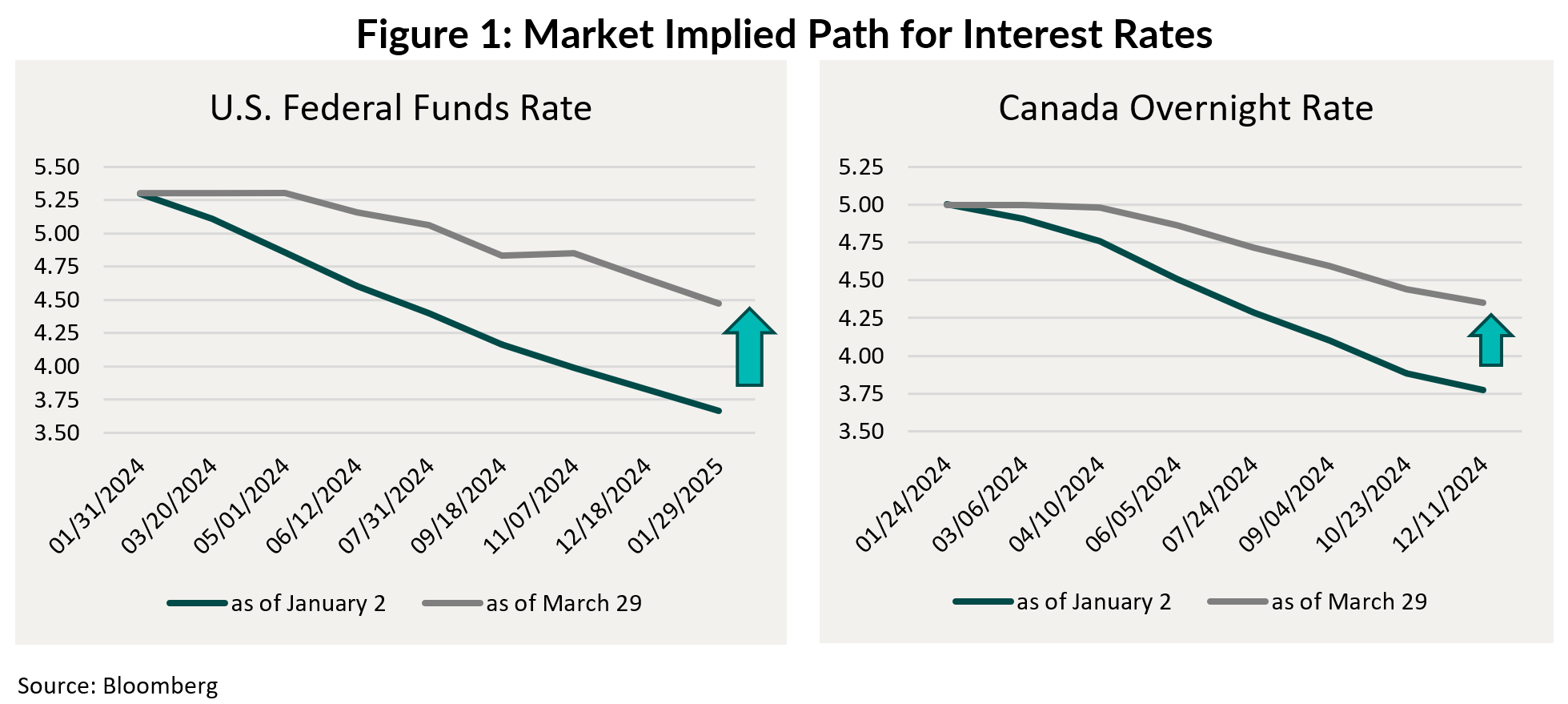

After getting overly excited about rate cuts at the start of the year, market sentiment has now gone full circle, discounting fewer and a much later start to rate cuts (Figure 1).

Both the Fed and BoC seem to agree, messaging in numerous speeches that it is still too soon to know with confidence if the recent improvement in economic activity and increase in inflation will be sustained. As we argued last month, services inflation remains too high for central bankers to bring overall inflation back to their 2% target in a timely fashion. Complicating their calculus even further, the recent increase in energy prices (WTI is over $85 a barrel as of the time of writing) risks increasing headline inflation even further in the months to come.

That leaves everyone, us included, waiting for the data to give us a sense of direction. So far this year, data has generally surprised mildly, and unevenly, to the upside (for example, the strong headline jobs gains in both countries in Jan and February, but an unexpected increase in unemployment). Even here in Canada, after showing no growth at all for most of last year, we had two strong months of GDP growth to start 2024. It has been a very mild winter, and some of this strength could be due to quirky seasonal adjustments. But overall the data has been better than we thought, and that means higher rates for longer. Risk assets are loving it, with equities close to all time highs and credit spreads back to their post pandemic lows. We continue to believe that the longer rates stay elevated, the more fragile the economy, and the more vulnerable it is to shocks. With credit priced to perfection, it is an easy decision for us to remain defensively positioned. In terms of interest rate risk, odds of further increases in rates are very low, but continued strong data could present upside risk to longer term rates. For now, we remain content to keep most of our rate exposure barbelled, with most of the portfolios exposed to 0-2 year rates (i.e. very little rate exposure), coupled with some long term government bond exposure (30 year) in case the economy flinches, necessitating deep and rapid rate cuts by central banks.

Credit

Canadian investment grade spreads took a breather in March after a strong start to the year. Spreads were flat on the month. For context, Canadian spreads remain 13bps tighter YTD, in line with US investment grade spreads (10bps tighter). The backdrop remains the same: risk assets continue to perform well while high all-in yields within corporate credit continues to attract capital. It should be no surprise that higher beta sectors continue to outperform more defensive sectors. Bank sub-debt (which we have been overweight for some time now) and REITs have been the star performers, while industrials, infrastructure, retail and utilities continue to lag (we own next to nothing within these sectors due to their generally rich valuations).

Even with the typical slower March (given Spring breaks), primary supply in Canada remained elevated. Canadian corporate issuance this past month clocked in at just shy of $13bln vs $8bln in 2023. This puts 2024Q1 issuance at $38bln in Canada, 60% ahead of this time last year. Even more impressive, 2024Q1 issuance is the second highest Q1 on record. As always, we use the primary market to deploy and recycle capital and this month was no different.

Individual fund commentary

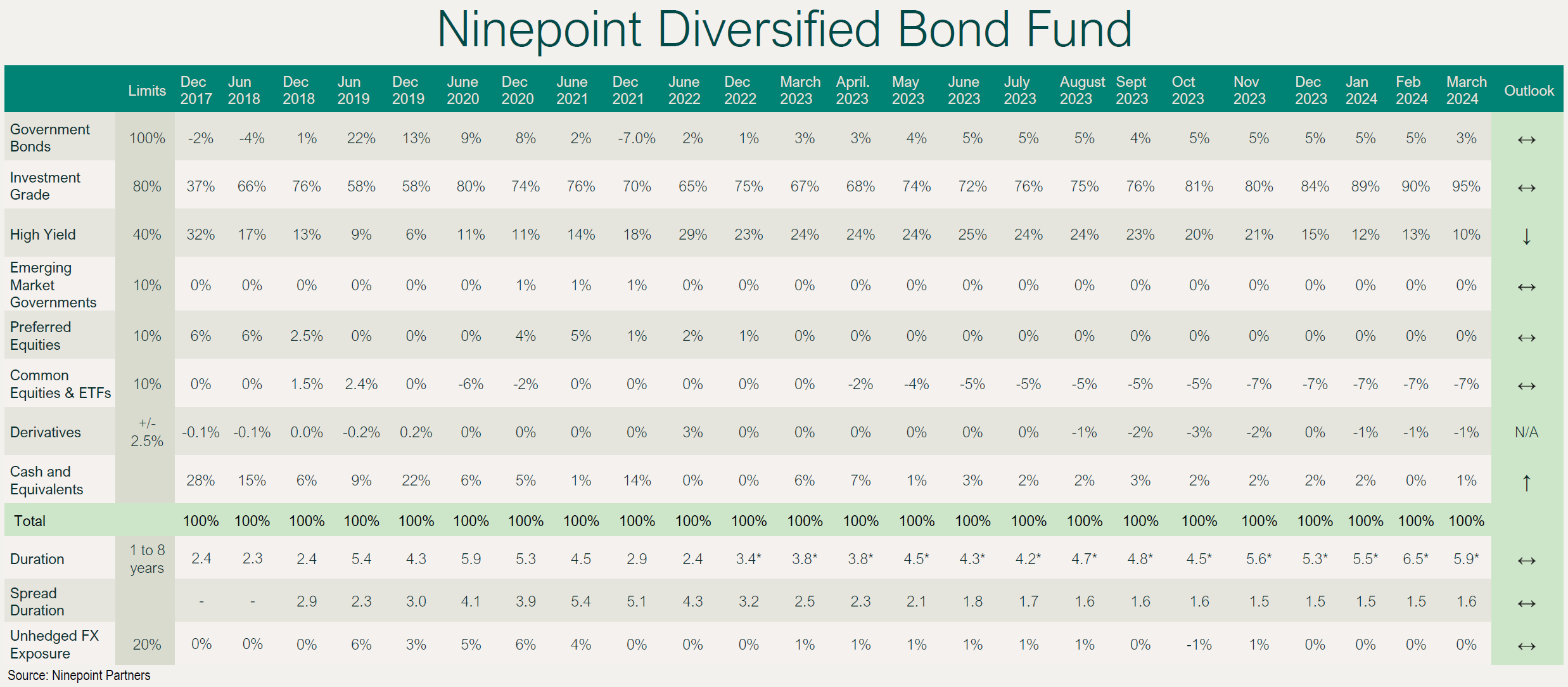

Ninepoint Diversified Bond Fund

The fund performed well this past month (+0.88%), and in 2024Q1 more generally (+1.08% YTD). Despite elevated interest rate volatility, we have benefited from strong income generation and capital gains in our LRCN/hybrid bond positions.

NINEPOINT DIVERSIFIED BOND FUND - COMPOUNDED RETURNS¹ AS OF MARCH 31, 2024 (SERIES F NPP118) | INCEPTION DATE: AUGUST 5, 2010

| 1M | YTD | 3M | 6M | 1YR | 3YR | 5YR | 10YR | Inception | |

| Fund | 0.9% | 1.1% | 1.1% | 7.1% | 5.2% | -0.7% | 1.0% | 2.3% | 3.2% |

There were no major changes to the fund’s defensive posture, other than duration being tweaked a touch lower to now sit at 5.9 years (vs 6.5 years last month as we took advantage of the increase in long term rates). Average credit quality remains unchanged at BBB+. Nonetheless, at 7.5%, the portfolio’s yield-to-maturity remains extremely compelling. The fund is mostly invested in shorter dated credit, so we will continue to have numerous maturities, which we use to source new opportunities, both in primary and secondary markets.

Speaking of opportunities, March was a very active month for Enbridge’s Commercial Paper program, a hidden gem in the Canadian market given its strong credit quality, very short tenors, and extremely high yields (mid 5%s). We tend to use this program to allocate cash as we wait to deploy capital.

Speaking of which, we participated in 3 new issues this month, all with coupons north of 5%: SNC Lavalin (a potential rising star), Royal Bank sub-debt (one of the rare parts of the market that still has value), and First National (a rare issuer who is extremely misunderstood by the Canadian market, hence the >6% coupon). Our HY weight declined from 13% to 10% given a Brookfield Property Finance (BPY) maturity, while our short position in HY (used for credit hedging purposes) remains at -7%. We are no longer exposed to BPY in any of our strategies.

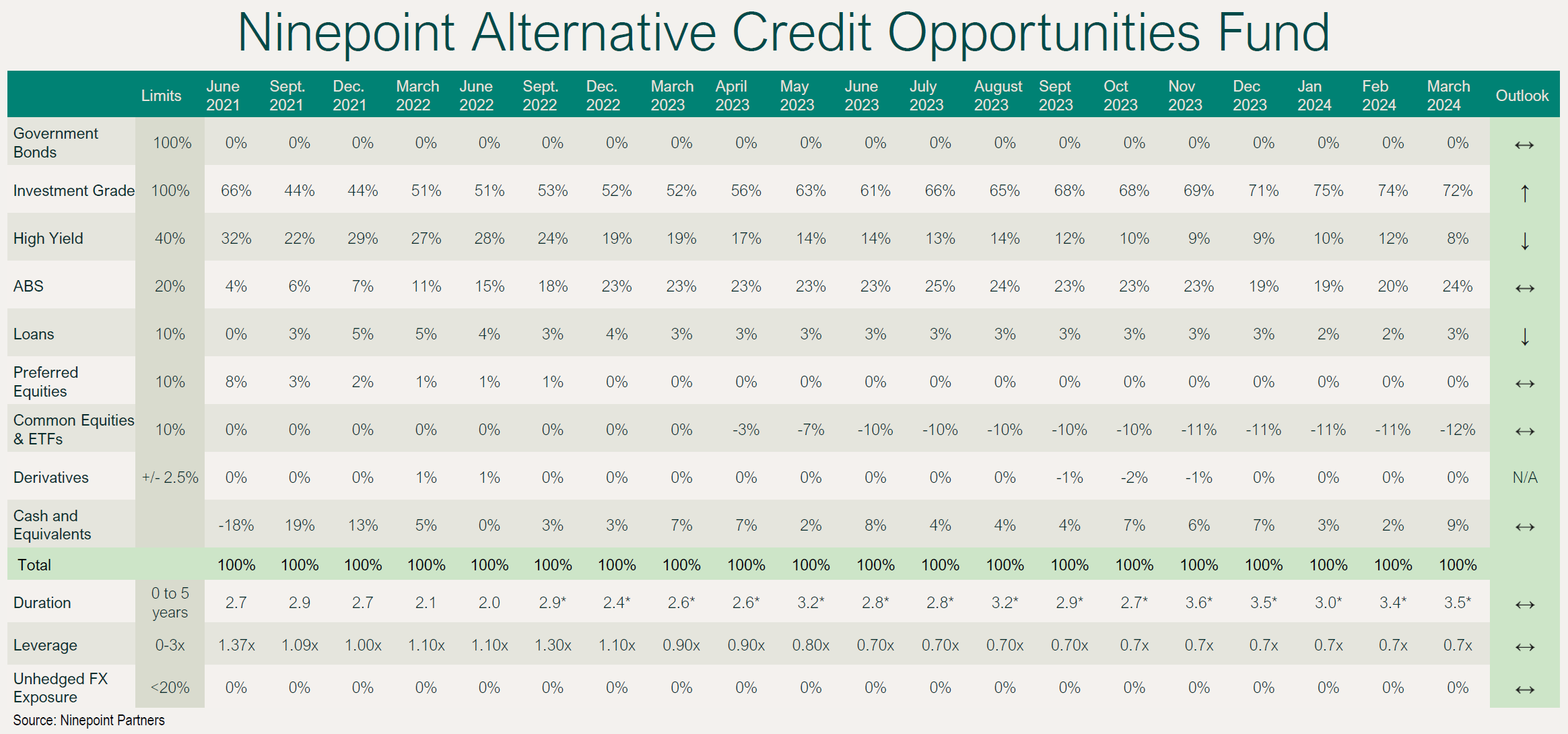

Ninepoint Alternative Credit Opportunities

Low interest rate exposure and solid income continue to benefit the fund, which returned 0.86% last month (2.38% YTD). Gains in Hybrids/LRCN more than offset our long-term government bond exposure.

NINEPOINT ALTERNATIVE CREDIT OPPORTUNITIES FUND - COMPOUNDED RETURNS¹ AS OF MARCH 31, 2024 (SERIES F NPP931) | INCEPTION DATE: APRIL 30, 2021

| 1M | YTD | 3M | 6M | 1YR | Inception | |

| Fund | 0.9% | 2.4% | 2.4% | 7.3% | 8.7% | 0.6% |

The portfolio’s characteristics remained broadly unchanged month-over-month. Duration ended at 3.5 years (vs 3.4 years the month prior), yield-to-maturity of 8.6% (flat vs prior month), spread duration of 3.2 years (slightly up from 3.1 years) and leverage unchanged at 0.7x. We sold some short dated SNC Lavalin’s to make room for their new issue. We also added to RY sub-debt at an attractive credit spread of 157 bps for a 5 year term. As mentioned last month, our high yield moved down on the month to 8% as our BPY maturity outweighed our SNC Lavalin purchase. Lastly, our short HY position (as a credit hedge) stayed at our target of -11%.

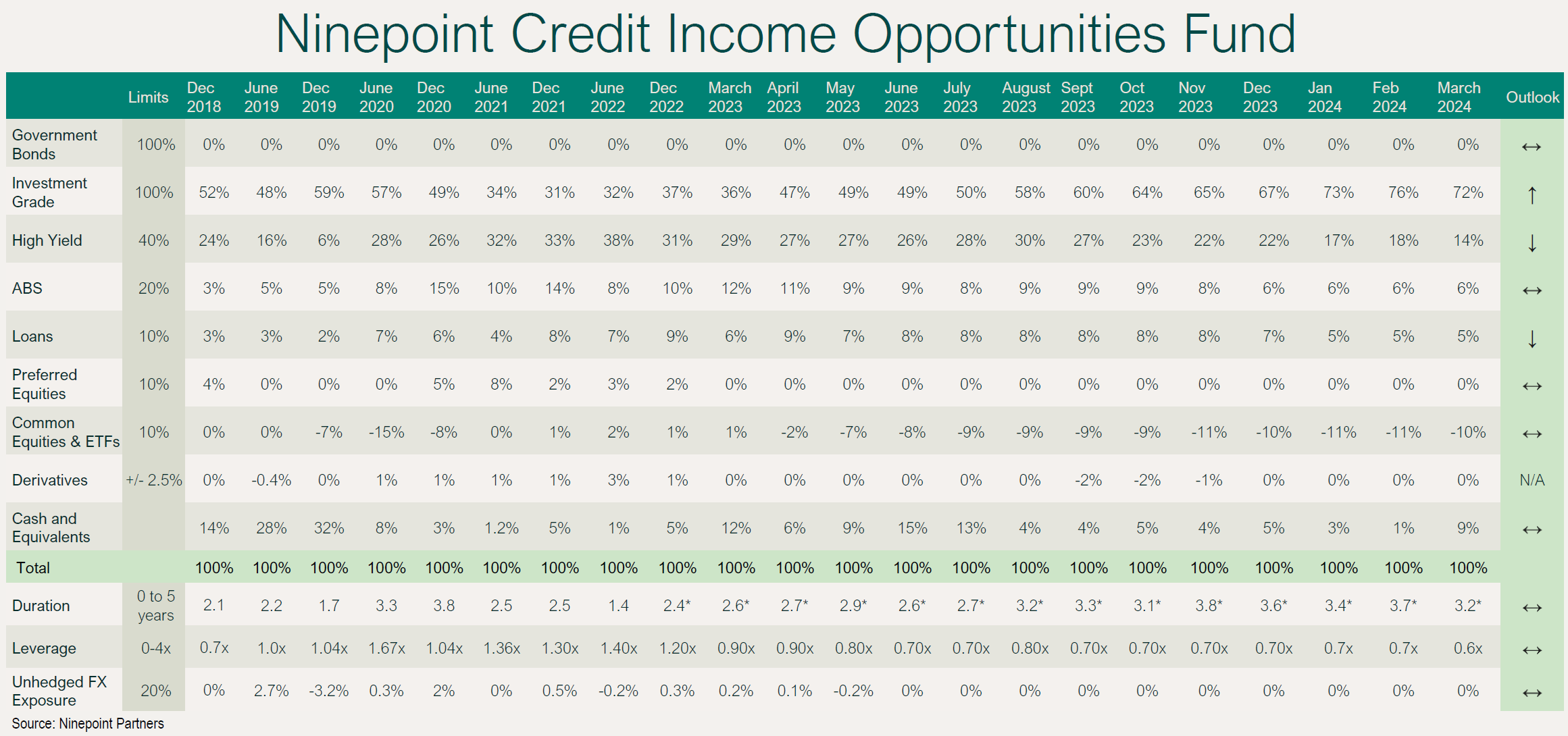

Ninepoint Credit Income Opportunities

Similar to the Alternative Credit Opportunities fund, it has been a good start to the year. The fund was up 0.87% in March (2.72% YTD), mostly driven by strong income generation and capital appreciation in Hybrids/LRCN.

NINEPOINT CREDIT INCOME OPPORTUNITIES FUND - COMPOUNDED RETURNS¹ AS OF MARCH 31, 2024 (SERIES F NPP507) | INCEPTION DATE: JULY 1, 2015

| 1M | YTD | 3M | 6M | 1YR | 3YR | 5YR | Inception | |

| Fund | 0.9% | 2.7% | 2.7% | 6.9% | 8.6% | 2.3% | 5.1% | 4.6% |

As of month-end, duration, yield-to-maturity, spread duration and leverage all remained broadly similar month-over-month, ending at 3.2 years, 9.2%, 3 years and 0.6x respectively. We believe these characteristics are prudent given our macroeconomic outlook. As the broad HY market remains extremely overvalued, we remain committed to our short HY position as the best way to hedge credit in an adverse environment. Similar to the other two funds, we added to RY sub-debt with a coupon north of 5%. Our high yield weight moved down on the month to 14% as our BPY maturity outweighed our SNC Lavalin purchase. We continue to exercise caution and recycle upcoming maturities in similarly high-quality paper.

Until next month,

Mark, Etienne & Nick

Ninepoint Partners

1 All Ninepoint Diversified Bond Fund returns and fund details are a) based on Series F units; b) net of fees; c) annualized if period is greater than one year; d) as at March 31, 2024 1 All Ninepoint Credit Income Opportunities Fund returns and fund details are a) based on Class F units; b) net of fees; c) annualized if period is greater than one year; d) as at March 31, 2024. 1 All Ninepoint Alternative Credit Opportunities Fund returns and fund details are a) based on Class F units; b) net of fees; c) annualized if period is greater than one year; d) as at March 31, 2024.

The Risks associated worth investing in a Fund depend on the securities and assets in which the Funds invests, based upon the Fund's particular objectives. There is no assurance that any Fund will achieve its investment objective, and its net asset value, yield and investment return will fluctuate from time to time with market conditions. There is no guarantee that the full amount of your original investment in a Fund will be returned to you. The Funds are not insured by the Canada Deposit Insurance Corporation or any other government deposit insurer. Please read a Fund's prospectus or offering memorandum before investing.

Ninepoint Credit Income Opportunities Fund is offered on a private placement basis pursuant to an offering memorandum and are only available to investors who meet certain eligibility or minimum purchase amount requirements under applicable securities legislation. The offering memorandum contains important information about the Funds, including their investment objective and strategies, purchase options, applicable management fees, performance fees, other charges and expenses, and should be read carefully before investing in the Funds. Performance data represents past performance of the Fund and is not indicative of future performance. Data based on performance history of less than five years may not give prospective investors enough information to base investment decisions on. Please contact your own personal advisor on your particular circumstance. This communication does not constitute an offer to sell or solicitation to purchase securities of the Fund.

Ninepoint Partners LP is the investment manager to the Ninepoint Funds (collectively, the “Funds”). Commissions, trailing commissions, management fees, performance fees (if any), other charges and expenses all may be associated with mutual fund investments. Please read the prospectus carefully before investing. The indicated rate of return for series F units of the Fund for the period ended March 31, 2024 is based on the historical annual compounded total return including changes in unit value and reinvestment of all distributions and does not take into account sales, redemption, distribution or optional charges or income taxes payable by any unitholder that would have reduced returns. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated. The information contained herein does not constitute an offer or solicitation by anyone in the United States or in any other jurisdiction in which such an offer or solicitation is not authorized or to any person to whom it is unlawful to make such an offer or solicitation. Prospective investors who are not resident in Canada should contact their financial advisor to determine whether securities of the Fund may be lawfully sold in their jurisdiction.

The opinions, estimates and projections (“information”) contained within this report are solely those of Ninepoint Partners LP and are subject to change without notice. Ninepoint Partners makes every effort to ensure that the information has been derived from sources believed to be reliable and accurate. However, Ninepoint Partners assumes no responsibility for any losses or damages, whether direct or indirect, which arise out of the use of this information. Ninepoint Partners is not under any obligation to update or keep current the information contained herein. The information should not be regarded by recipients as a substitute for the exercise of their own judgment. Please contact your own personal advisor on your particular circumstances. Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any investment funds managed by Ninepoint Partners LP. Any reference to a particular company is for illustrative purposes only and should not to be considered as investment advice or a recommendation to buy or sell nor should it be considered as an indication of how the portfolio of any investment fund managed by Ninepoint Partners LP is or will be invested. Ninepoint Partners LP and/or its affiliates may collectively beneficially own/control 1% or more of any class of the equity securities of the issuers mentioned in this report. Ninepoint Partners LP and/or its affiliates may hold short position in any class of the equity securities of the issuers mentioned in this report. During the preceding 12 months, Ninepoint Partners LP and/or its affiliates may have received remuneration other than normal course investment advisory or trade execution services from the issuers mentioned in this report.

Ninepoint Partners LP: Toll Free: 1.866.299.9906. DEALER SERVICES: CIBC Mellon GSSC Record Keeping Services: Toll Free: 1.877.358.0540

Related Funds

Historical Commentary

- Fixed Income Strategy 12/2023

- Fixed Income Strategy 11/2023

- Fixed Income Strategy 10/2023

- Fixed Income Strategy 09/2023

- Fixed Income Strategy 08/2023

- Fixed Income Strategy 07/2023

- Fixed Income Strategy 06/2023

- Fixed Income - H1 2023 Market Review and Outlook

- Fixed Income Strategy 05/2023

- Fixed Income Strategy 04/2023

- Fixed Income Strategy 03/2023

- Fixed Income Strategy 02/2023

- Fixed Income Strategy 01/2023

Toronto, Ontario M5J 2J1 Canada