How shifting reserve behavior, tighter supply conditions, and improving equity fundamentals are reshaping the sector’s risk-reward profile.

Today’s markets are being shaped by a complex mix of geopolitical shifts and long-term supply pressures. Against this backdrop, precious metals warrant a closer look, not just as a short-term hedge against volatility, but as a structural component of a modern, diversified portfolio.

Gold: Moving from Tactical Hedge to Strategic Asset?

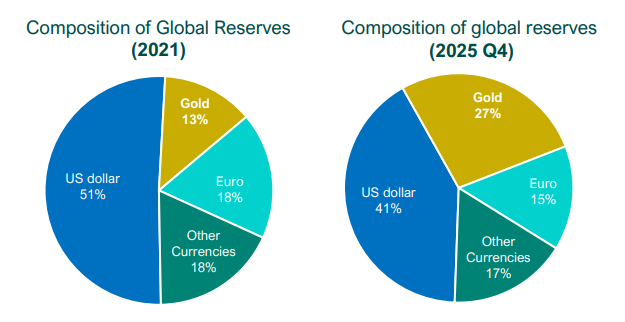

The current gold cycle appears to have gained real traction in early 2022, when a change in global reserve management began to take hold. Since then, central banks, particularly in emerging markets, have been consistent buyers of physical gold.

That demand matters because it is different from more traditional investor flows. It is less sensitive to short-term price movement and more closely linked to long-term objectives such as reserve diversification, reduced reliance on the U.S. dollar, and greater geopolitical flexibility. It also helps explain why gold has remained resilient through periods of broader market stress.

This may represent an important shift. Gold has often been discussed primarily as a tactical hedge: useful during episodes of instability, but harder to justify as an enduring allocation. Today, the case appears to be evolving. If official-sector buying remains a durable feature of the market, gold may increasingly merit consideration as a strategic diversifier within portfolios rather than simply a temporary defensive trade.

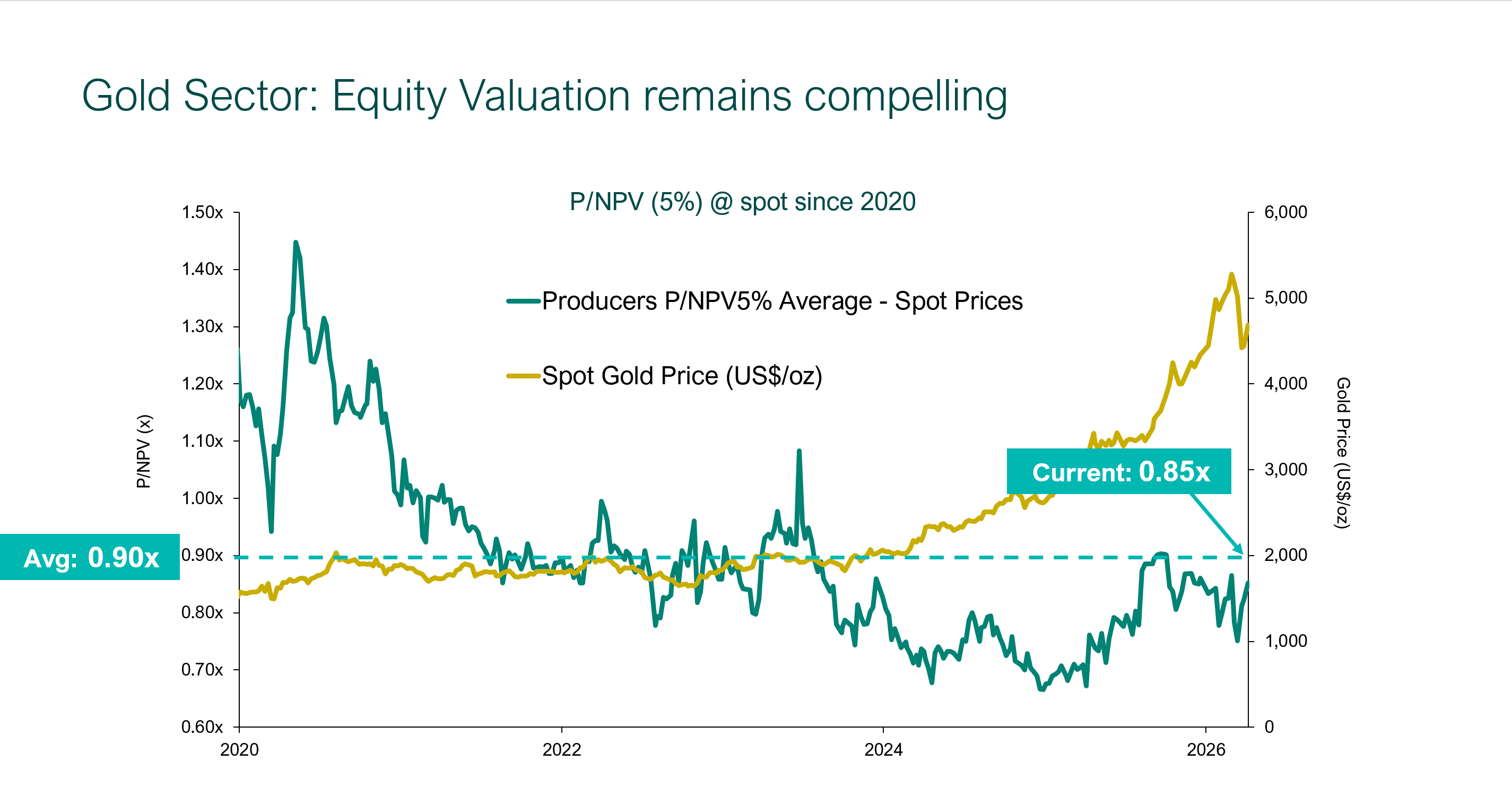

Gold Equities: Improved Fundamentals, Limited Rerating

If bullion has been resilient, gold equities have been comparatively restrained.

That gap is notable. At current gold prices, many producers are generating strong free cash flow, carrying healthier balance sheets, and demonstrating more disciplined capital allocation than in prior cycles. Share buybacks have also become a more meaningful use of excess cash flow. Yet despite this improvement, equity valuations remain relatively subdued.

The distinction between bullion and equities is important. Physical gold may serve as a source of resilience and diversification. Gold equities, by contrast, can offer exposure to improving operating fundamentals, margin expansion, and the potential for valuation rerating if capital flows return more meaningfully to the sector.

Those are not interchangeable roles. Treating precious metals as a single exposure can obscure the different functions they may serve within portfolios.

Volatility May Be a Feature, Not a Thesis Breaker

Recent market action has been a reminder of how quickly macro narratives can shift. Geopolitical tension, higher energy prices, fading expectations for rate cuts, U.S. dollar strength, and broad-based risk reduction have all contributed to weakness in equities, including at times in precious metals and mining shares.

But short-term price pressure does not necessarily invalidate the broader case.

The more important question is whether the structural drivers have materially changed. So far, they do not appear to have. Central bank demand remains intact. The macro case for diversification remains relevant. And the disconnect between commodity prices and mining-equity valuations remains notable.

For advisors, that distinction matters. In volatile markets, it is easy for short-term dislocations to dominate the conversation. In practice, those periods often say more about liquidity and positioning than they do about the durability of the underlying thesis.

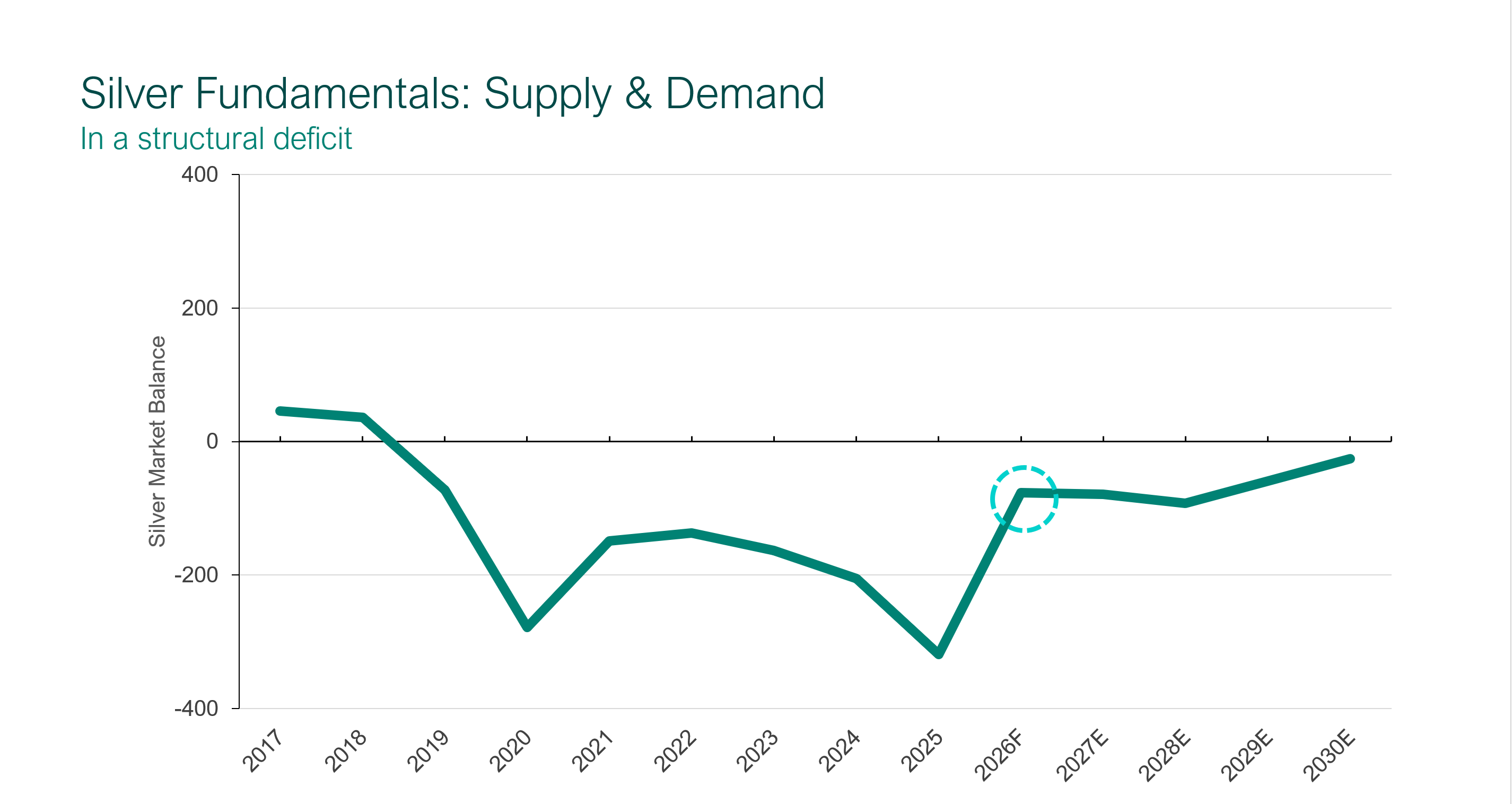

Silver: A Different Kind of Exposure

Silver also deserves separate consideration.

Unlike gold, silver sits at the intersection of monetary demand and industrial demand. That makes it inherently more volatile, but it also gives it a broader range of potential drivers.

For years, silver prices remained below levels that would meaningfully support new supply growth. At the same time, industrial demand has expanded, driven by themes such as solar, electrification, and emerging technologies. The result has been a persistent supply deficit and a tightening physical market.

For advisors, silver may therefore represent a different type of portfolio exposure than gold. Gold may be the cleaner strategic reserve asset. Silver may offer greater sensitivity to both macro instability and long-term industrial demand growth. That combination can make it less purely defensive, but potentially more responsive in an environment where physical tightness persists.

Mining More Broadly: Increasingly Tied to Structural Demand

The broader metals and mining complex is also changing in ways that may become more relevant for portfolios.

Demand is no longer being driven solely by traditional cyclical forces. It is increasingly linked to longer-duration structural themes: electrification, energy transition, AI infrastructure, supply-chain resiliency, national security, and resource independence. In many cases, supply is not simply responding to growth, it is becoming a constraint on it.

That backdrop has important implications. Mining remains a cyclical and operationally complex sector, but it is also becoming more directly connected to strategic economic priorities. That shift may not eliminate volatility, but it does change how the sector can be framed. In a world where access to critical materials is becoming more important, selected mining exposures may warrant more attention than they have historically received.

What This May Mean for Investors

For investors, the implication is not that portfolios should become aggressively positioned around commodities. Rather, it is that precious metals and mining may deserve a more nuanced and intentional review.

A few portfolio considerations stand out.

Physical gold and precious metals equities may serve complementary rather than interchangeable roles. Gold may be increasingly relevant as a strategic diversifier in a world defined by reserve fragmentation, policy uncertainty, and geopolitical stress. Gold equities may offer leverage to improved fundamentals that are not yet fully reflected in valuations. Silver may provide exposure to both monetary demand and structural industrial tailwinds. Broader mining exposures may increasingly intersect with long-term themes around energy, infrastructure, and security.

Viewed through that lens, the conversation is not simply about whether precious metals rise from here. It is about whether the drivers behind the space are becoming more durable and whether portfolios are positioned in a way that reflects that possibility.

A Case for Reassessment

Precious metals are operating within a backdrop that remains volatile, but increasingly supportive on a structural basis. Gold is being accumulated in a way that suggests strategic intent. Silver continues to face a tighter physical market. Mining equities, in many cases, are showing stronger fundamentals than current valuations appear to recognize.

For investors, this may not be a call for aggressive positioning. It may, however, be a timely case for reassessment. In a market environment increasingly shaped by fragmentation, resource constraints, and shifting policy priorities, precious metals and mining exposures may warrant a more intentional role than they have in recent years.