April 30, 2026

April 30, 2026

Commentary

The monthly commentary discusses recent developments across the Ninepoint Diversified Bond, Ninepoint Alternative Credit Opportunities and Ninepoint Credit Income Opportunities Funds.

Another year, another set of unexpected challenges. This time it’s not Liberation Day and a global trade war, but instead a real war in the Middle East. In the context of the global economy, Iran and the Strait of Hormuz are hugely consequential; a large share of the global oil, liquefied natural gas, petrochemicals, aluminum and fertilizers transit through there. With the Strait closed for several months, the world is now faced with higher prices for all those commodities and products, along with lost output due to shortages of those same commodities.

The U.S. administration is stuck between a rock and a hard place. The Iranian regime has a much higher pain tolerance than the average American voter, and with the midterms coming up in the Fall and energy prices still very high (and at the risk of going higher if the Strait doesn’t reopen soon), the race is on to find a face saving way to end the conflict. The problem is, the Iranians know this, and are playing hardball. So, the “base case” assumption in markets right now is that we are on the edge of a reopening of Hormuz comes with very wide uncertainty bands; this conflict could go on for much longer, with devastating consequences for the global economy.

However, the pain is not spread evenly. While North America is generally well endowed with energy, the same cannot be said of Europe and Asia, who are net importers. The availability of energy is therefore what distinguishes those who “only” face higher prices, with those who must both pay higher prices, but are also impacted by a shortage of energy and resources that will curtail economic activity. Already, places like Australia are facing product shortages, and have had to hike interest rates to fight inflation. In Europe, both the ECB and BoE are also preparing the market for rate hikes as soon as June.

This is a particularly complex problem for central banks: higher prices (inflation) and lower growth are not problems that interest rates are well-suited to solve. In general, common practice is to look-through temporary jumps in commodity prices, since raising rates to quash aggregate demand and return inflation to target is seen as counter-productive. But some countries have had inflation above target for several years now, and exceptional circumstances such as the AI CAPEX boom in the U.S., along with goods price increases from the 2025 tariffs, are all pushing prices and inflation well to the upside.

This might leave the Fed little choice but to raise rates, embarking on another rate hike cycle. Although this will all depend on the length of the conflict, the longer it lasts, the more likely higher energy prices spread through to other prices, increasing not just the level, but the breadth of inflation. Once that process starts, as we saw it in 2022, it requires a heavy dose of monetary tightening to stop the bleeding. At the very least, we should expect the Fed to be on hold for the balance of the year.

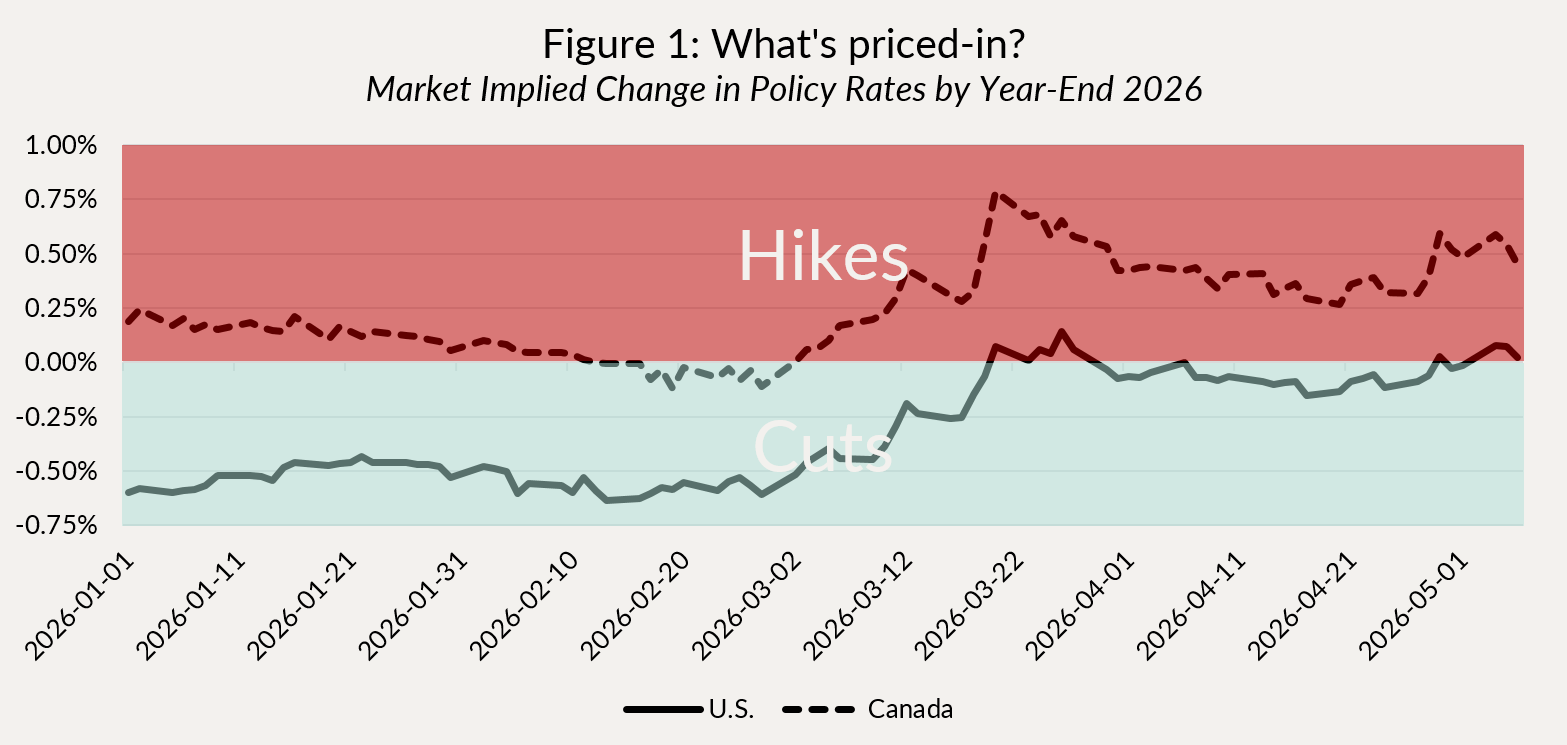

Contrast this backdrop with the market’s (misguided) expectations for U.S. rate cuts at the beginning of 2026 (Figure 1), it is no surprise that bond yields across the yield curve have moved significantly higher.

Here in Canada, the BoC has a stronger hand going into this energy crisis. There is slack in the economy, unemployment is higher, inflation has been around target for more than a year, and core inflation was on a downward trend, prior to the war. This will allow the BoC to be patient, but just like in the U.S., if the energy shock persists and starts spreading to core inflation, then they will have to act, embarking on a “series of rate hikes”, as Governor Macklem recently said.

Click for larger image

Following the start of hostilities, the bond market was quick to react, pricing as many as 3 (75 basis points) rate hikes in Canada by the end of the year (Figure 1). Assuming a long tail to the conflict, that seems about right. Should it be resolved sooner, it is also possible that the Bank remains on hold for the balance of the year, which was our assumption prior to the conflict. Given the constant stream of conflicting headlines on social media, interest rates (and expectations for hikes) have moved around a lot, demanding us to have a nimble approach to duration management over the past few months. Too few hikes (or outright cuts like in the U.S.) priced-in means bonds are expensive, which we have bet against, whereas too many hikes (i.e. as many as 3 in Canada) means bonds are cheap, and present a good entry point to add duration. We aren’t usually that active trading interest rates, but this environment has proven to be very well suited to it.

So on balance, a fairly bad inflation outcome was already priced-in the Canadian curve (close to 3 hikes in 2026, which has since faded ), whereas in the U.S, with inflation already above target and the price pressures stemming from AI, energy and tariffs, we see risk to the upside (i.e. higher rates, lower bond prices), particularly in the front end and belly of the curve, which are more sensitive to changes in monetary policy. We are therefore positioning accordingly: there is no telling when this war will end, so generally a low duration bias is appropriate. We have also used options on interest rates to manage those wild swings in monetary policy expectations (and interest rates) due to the conflict and oil price gyrations, lowering fund volatility and collecting additional income.

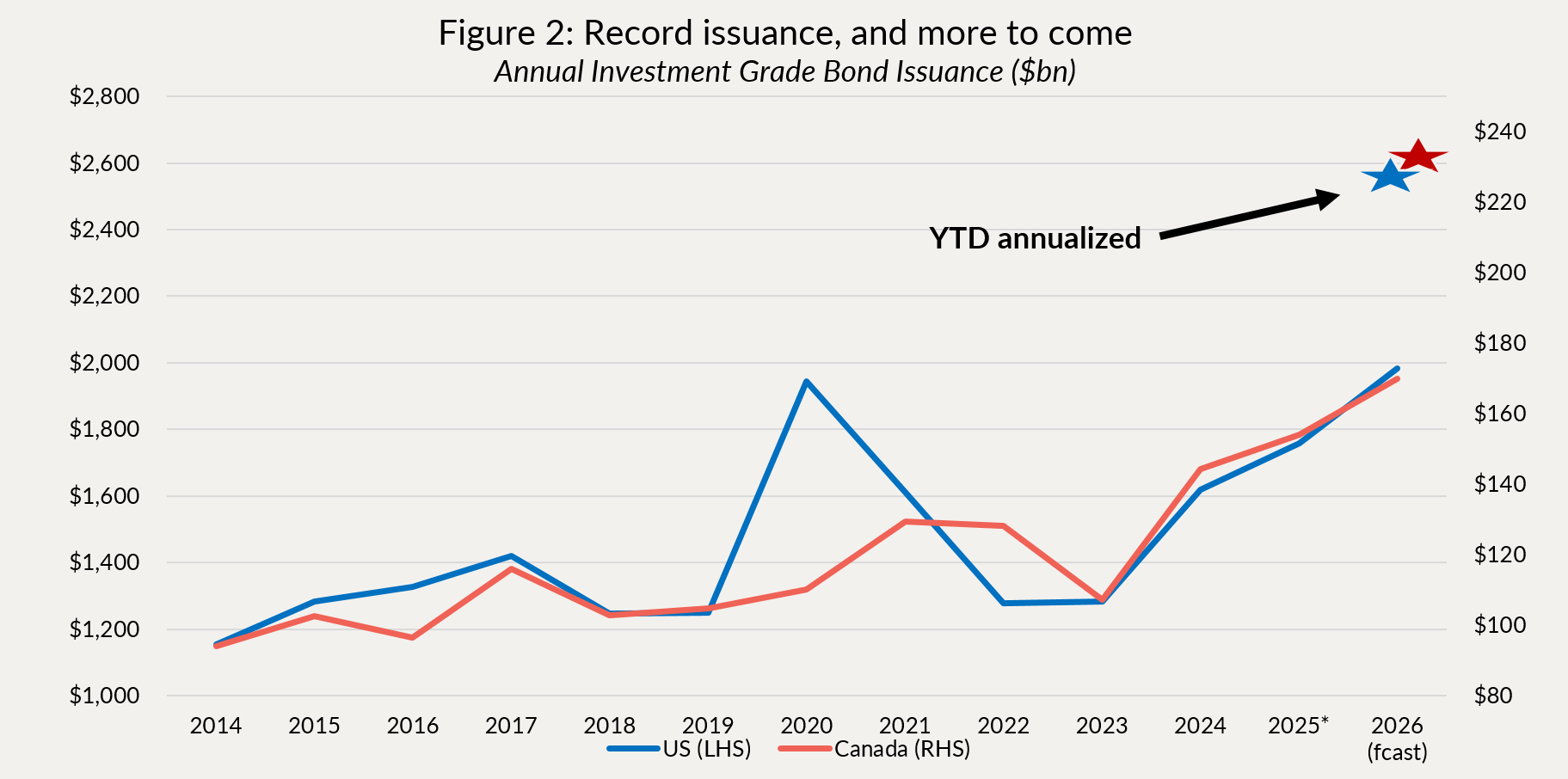

Turning to credit markets, 2026 has so far played out as we expected. Spreads were at multi-decade lows and new issue activity has been off the charts, leading to a progressive repricing wider of the credit market. It started with AI hyperscalers having massive funding needs and this has led to record new issue activity in the U.S. investment grade corporate bond market. With the Canadian market still relatively cheap for companies to issue bonds (versus the U.S.), we have seen a wave of maple issuers here (non-domestic issuers). In May, our first hyperscaler (Google) printed the largest ever corporate bond deal in Canada, at $8.5bn. And its not over, we expect this to continue. Total new issuance year-to-date is tracking 200% above last year in the Canadian market, and plus 28% in the (much larger) US market (Figure 2 below shows annual investment grade issuance along with this year’s pace, which could break records).

Click for larger image

So, barring any further deterioration in the economic outlook or headlines related to private credit, our view is that corporate credit spreads will continue to modestly widen as the market digests this unprecedented wave of corporate new issues. Should some of the downside to economic growth (and upside inflation) scenarios come to pass, then expect corporate credit to sell off more meaningfully.

Given all of this, we have remained defensively positioned in credit. Our credit duration is low, due to both positioning and credit hedges. Similar to how we have managed the interest rate volatility, we are using credit derivatives to protect against the market gyrations, hedging the portfolios through periods of volatility, while generating some additional income for the funds.

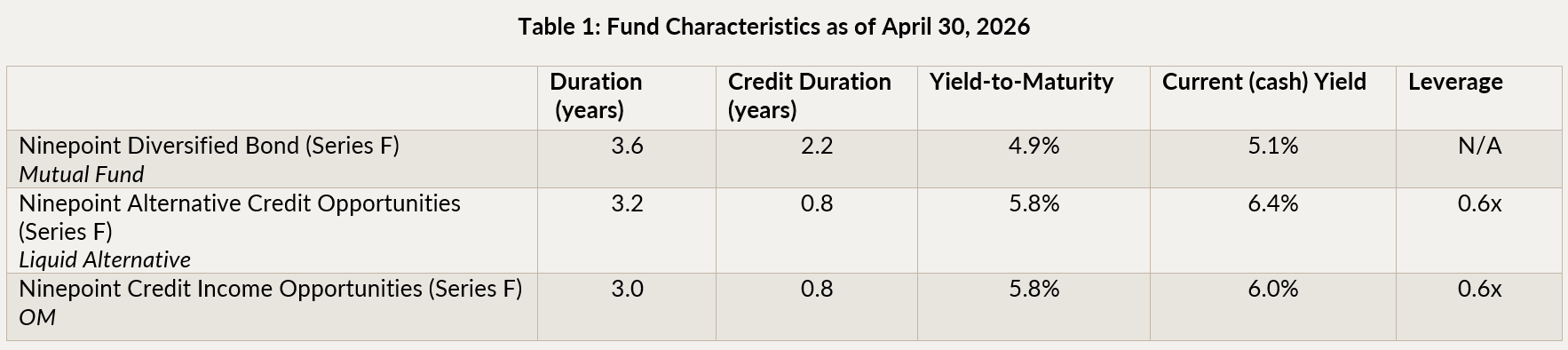

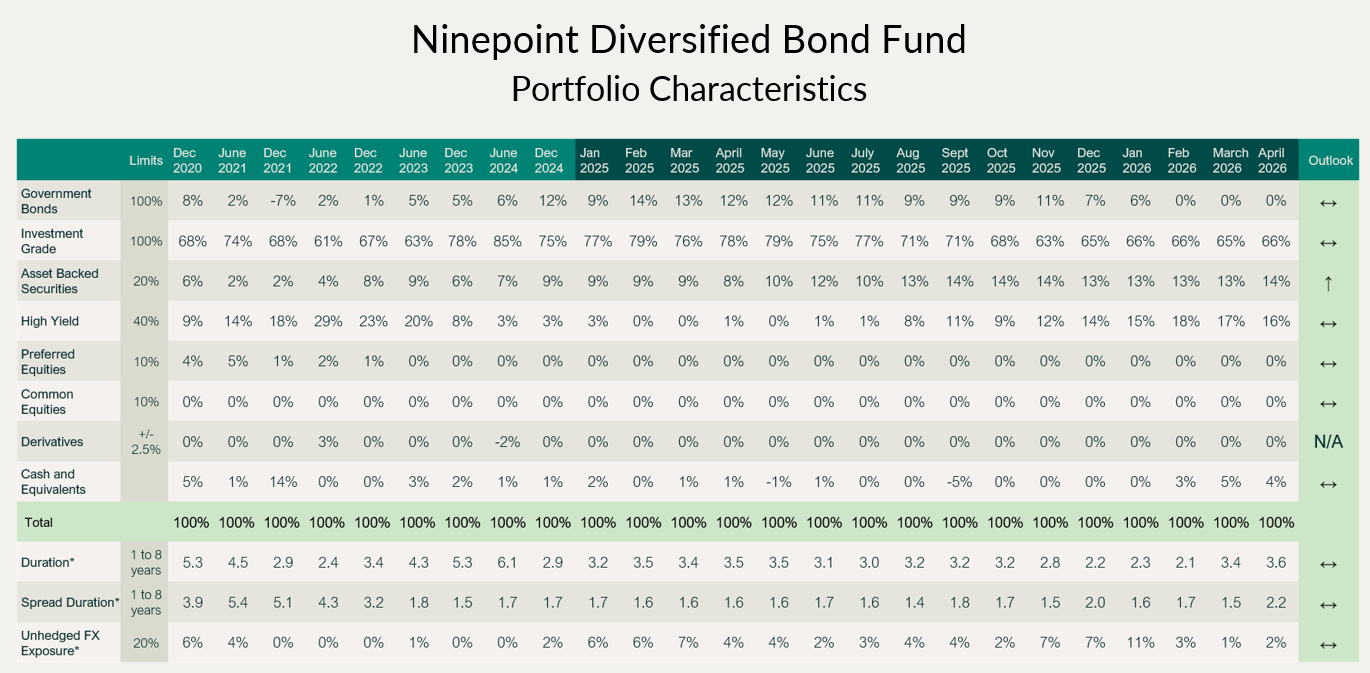

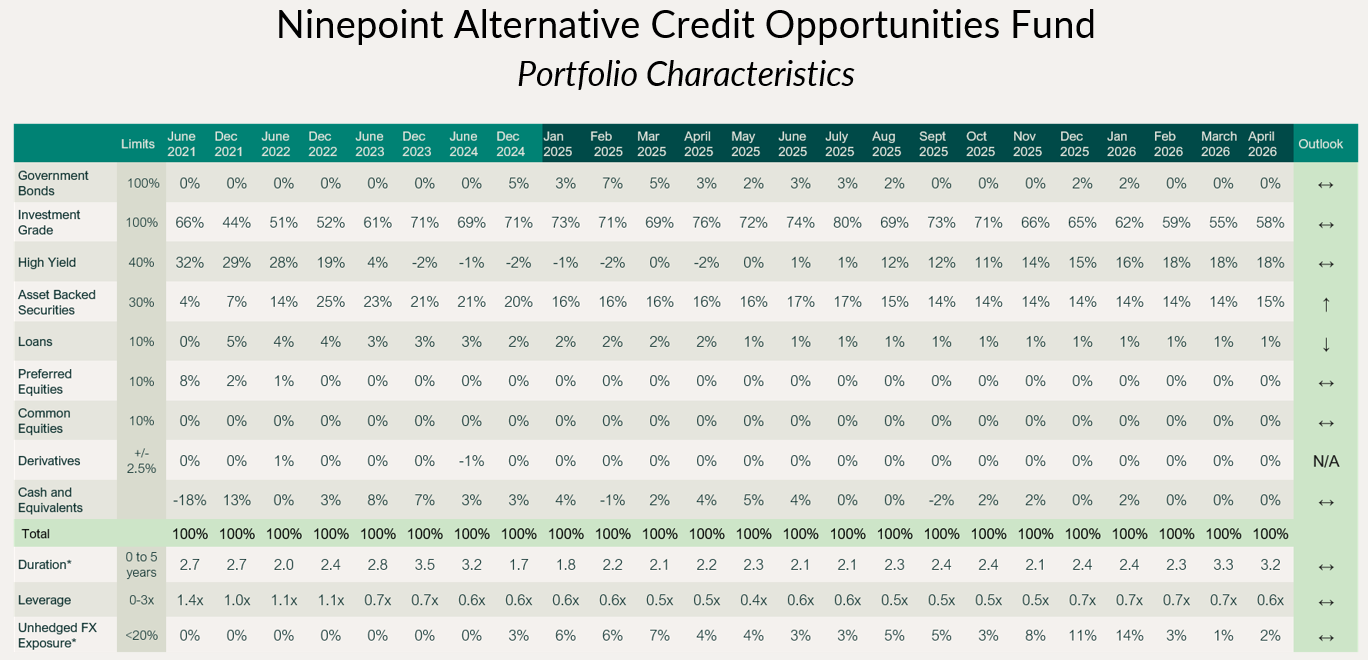

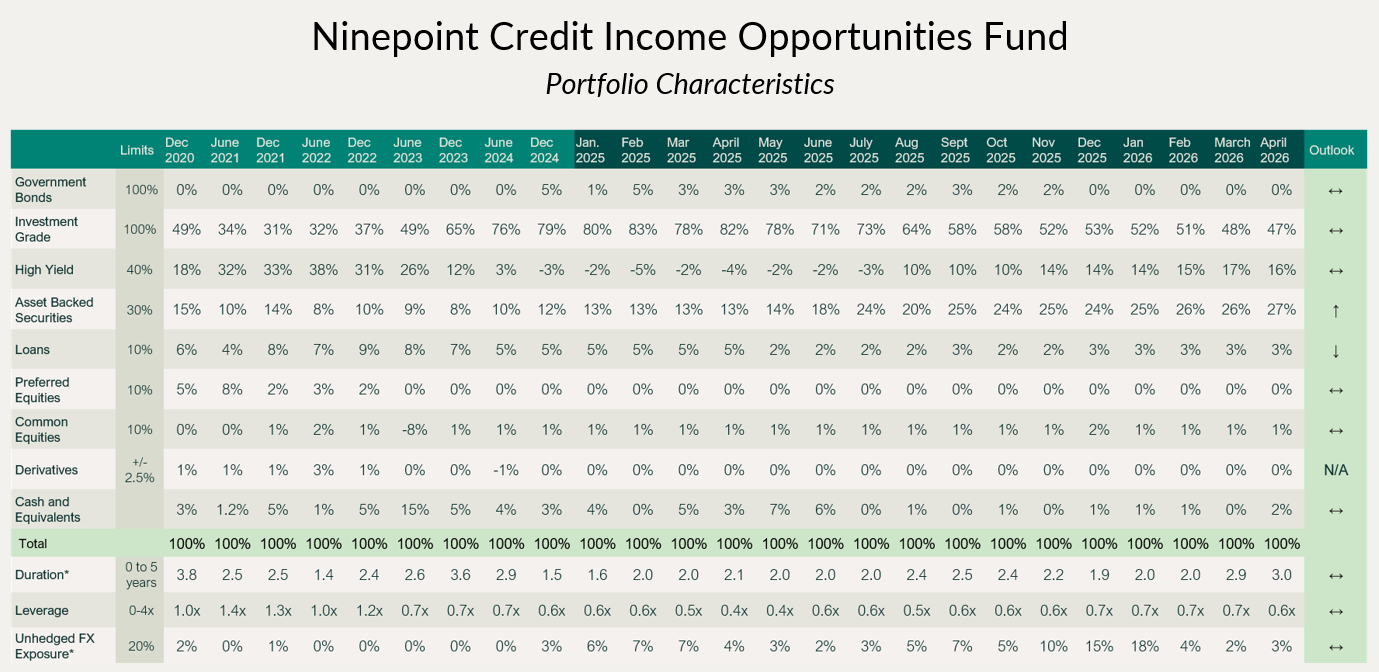

Table 1 below shows the various statistics and exposures as of month end. As described above, duration went up a smidge since March, to just over 3 years, while spread/credit duration remained very low, due to the impact of credit hedges.

Click for larger image

Portfolio yields remain healthy, ranging from 5-6%, despite our defensive posture. This is primarily related to security selection; late last year, we sourced attractive hybrid bonds ($C and USD market) and asset backed securities ($C market mostly) that provide elevated yields, low duration, and, in our view, resilience to credit stress, as was witnessed most recently during the volatility in March.

Conclusion

Despite all the volatility, the portfolios have behaved well. As the potential range of economic outcomes continue to be wide, we intend to manage rate and credit risks tightly. We believe our current portfolio positioning is appropriate, but as always, we are ready to adjust our positioning, should things change materially.

Ninepoint Diversified Bond Fund

NINEPOINT DIVERSIFIED BOND FUND - COMPOUNDED RETURNS¹ AS OF APRIL 30, 2026 (SERIES F NPP118) | INCEPTION DATE: AUGUST 5, 2010

1M |

YTD |

3M |

6M |

1YR |

3YR |

5YR |

10YR |

15YR |

Inception |

|

|---|---|---|---|---|---|---|---|---|---|---|

Fund |

0.32% |

0.97% |

0.53% |

1.10% |

3.46% |

5.55% |

1.86% |

2.88% |

3.18% |

3.56% |

Click for larger image

Ninepoint Alternative Credit Opportunities Fund

NINEPOINT ALTERNATIVE CREDIT OPPORTUNITIES FUND - COMPOUNDED RETURNS¹ AS OF APRIL 30, 2026 (SERIES F NPP931) | INCEPTION DATE: APRIL 30, 2021

1M |

YTD |

3M |

6M |

1YR |

3YR |

Inception |

|

|---|---|---|---|---|---|---|---|

Fund |

0.32% |

0.92% |

0.41% |

1.05% |

4.26% |

6.86% |

2.87% |

Click for larger image

Ninepoint Credit Income Opportunities Fund

NINEPOINT CREDIT INCOME OPPORTUNITIES FUND - COMPOUNDED RETURNS¹ AS OF APRIL 30, 2026 (SERIES F NPP507) | INCEPTION DATE: JULY 1, 2015

1M |

YTD |

3M |

6M |

1YR |

3YR |

5YR |

10YR |

Inception |

|

|---|---|---|---|---|---|---|---|---|---|

Fund |

0.38% |

0.85% |

0.55% |

1.17% |

4.27% |

6.75% |

3.75% |

5.39% |

4.88% |

Click for larger image

Good luck and until next month.

Mark, Etienne & Nick

As always, please feel free to reach out to your product specialist if you have any questions.