May 31, 2026

May 31, 2026

Commentary

The monthly commentary discusses recent developments across the Ninepoint Diversified Bond, Ninepoint Alternative Credit Opportunities and Ninepoint Credit Income Opportunities Funds.

For those that are counting, it has now been (at the time of writing) the 38th time that we “have a deal” with Iran. Granted, this time it does feel like we are getting close to an interim agreement for a ceasefire and to reopen the Strait of Hormuz, with a 60-day timeline to resolve the thornier issues, with Iran’s nuclear program the main sticking point. The situation will remain fragile until it’s all settled, and we should expect this process to be volatile. In the meantime, the equity and credit markets are behaving as though the situation is back to normal. Central banks and government bond markets, by contrast, remain more cautious.

Starting with central banks, we have heard from both the Bank of Canada (BoC) and the ECB in the first week of June. Both were as expected. The ECB is the first major central bank to hike following the energy shock. Inflation, both headline and core, has moved higher and due to their reliance on energy from the Gulf, and they therefore felt like they needed to act to solidify their credibility. We would not be surprised if they hiked again in July.

Here in Canada, the situation is a little different, which affords the BoC some time. Inflation has been at target for more than a year, and the economy is soft due to a variety of factors (weak housing market, negative population growth, trade uncertainty depressing investment), so domestic inflation pressures are well contained. This allows them, for now, to look through the jump in energy prices, and see how this plays out. As long as the increase in energy prices doesn’t spread to other prices, there is no need to be pre-emptive like the ECB and hike our economy into a recession. Our base case is that the BoC doesn’t hike this year, but continues to message their readiness to hike, as a way to maintain inflation expectations anchored. This is their best strategy here. Of course, if the situation in the middle east doesn’t get resolved at all by the Fall, then we risk another jump higher in energy prices, at which point it might be harder for them to stay on the sidelines, and another, hugely detrimental to economic growth, rate hike cycle might begin. Given this risk, we believe that it is prudent to keep duration low across the funds, particularly now that the bond market is pricing less than 20bps of hikes in Canada by the end of the year.

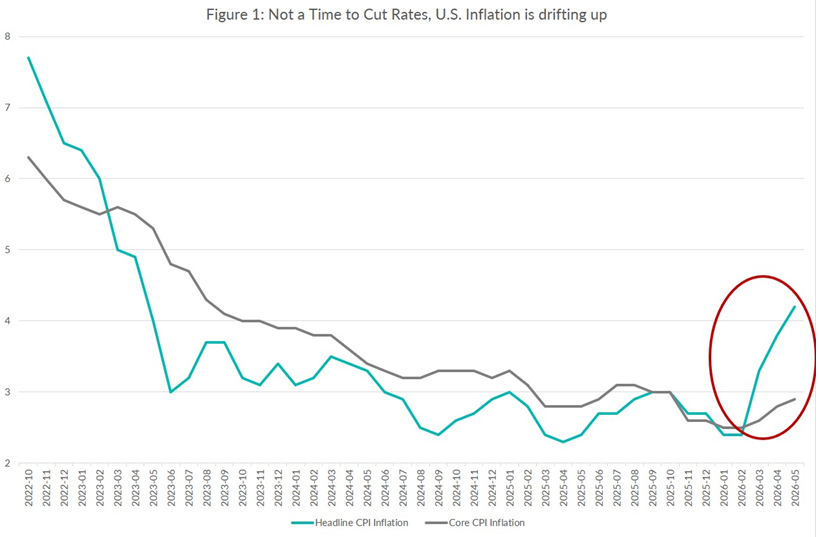

In the U.S., we have a change of leadership at the Fed, with Kevin Warsh set to start his Chairmanship at the June FOMC meeting. It is a tricky time to be a central banker, and particularly in the U.S., where inflation has been reaccelerating. If it was only energy prices because of the war in Iran, they could look through it, but tariffs and AI CAPEX are also pushing inflation higher, so it becomes harder to dismiss inflation as “transitory”.

Click for larger image

The bond market has completely shifted its stance. While at the start of 2026, it was expecting 2 rate cuts this year, it now prices a rate hike, and more next year as well. That’s a problem for Mr. Warsh, who’s just been appointed by a president that demands easier monetary policy. How will he square that circle? His first FOMC press conference will be quite interesting. We suspect that this tug of war between the new Fed Chair and the bond market won’t be resolved that quickly, and with that, we should see some volatility in U.S. rates. We are therefore keeping our U.S. duration exposure to a minimum. We do have some positions in U.S. bonds, but they are either rates-hedged (and currency hedged for that matter), or they are very short dated (2 years and less).

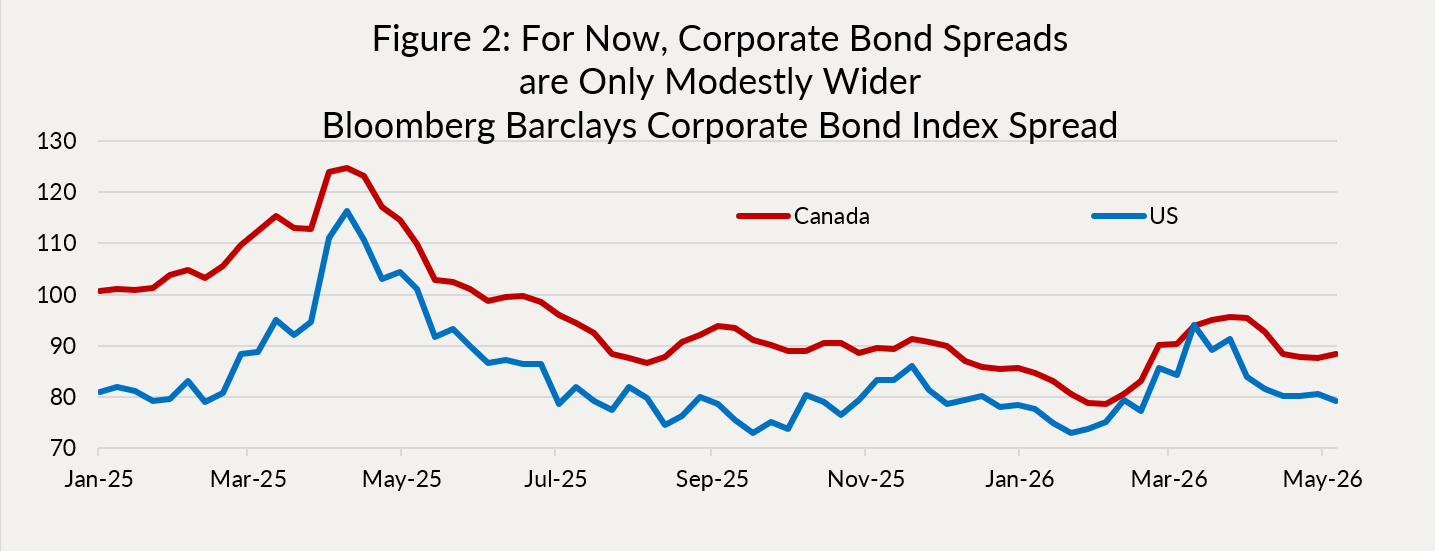

Turning to credit, so far this year it’s been like drinking from a firehose. Canada is definitely open for business. We have had record issuance (up 60% vs the same time last year, and last year was a record year), and so far it has been well absorbed by the market. That is, until the Amazon mega deal the first week of June, which printed $14bn, eclipsing the $8.5bn record that Google had set the month before. Once again, the majority of the paper came with long term tenors (10 and 30 years), which has put pressure on that part of the credit curve. We saw both steepening and widening of higher quality corporates. We do have some relative value trades in our alternative strategies to benefit from this decompression of corporates to provincials.

But overall, given the amount of bonds, the market has absorbed this supply surprisingly well, and investment grade credit spreads remain very close to post-GFC lows (Figure 2). Issuance wise, we expect to see more of the same, as Canada now has established itself as a prime diversification destination for large foreign companies looking for investment grade funding. And they do need a lot of funding, as it seems CAPEX expectations from AI hyperscalers and other related companies keeps pushing higher.

Click for larger image

With spreads this tight, we remain cautious on credit, simply because there’s only so far they can rally from here. Nonetheless, there is always something interesting to buy. We always scour the market for opportunities, and these days we mostly find them in Canadian Asset Backed Securities (credit cards, personal loans, commercial and residential mortgages, data centers, etc), where we can find attractive spreads (100-150basis points), low duration (2 to 5 years), and reasonably high credit quality (A to AAA). Why is this so cheap? For one, it’s not part of the index, attracting less demand, and most of these issues are small, so they wouldn’t move the needle for our larger competitors. So expect us to continue slowly increasing our allocation to this asset class. Due to their lower liquidity profile (impossible to find in secondary markets), we usually buy small weights (1-3%) and ladder them across the funds.

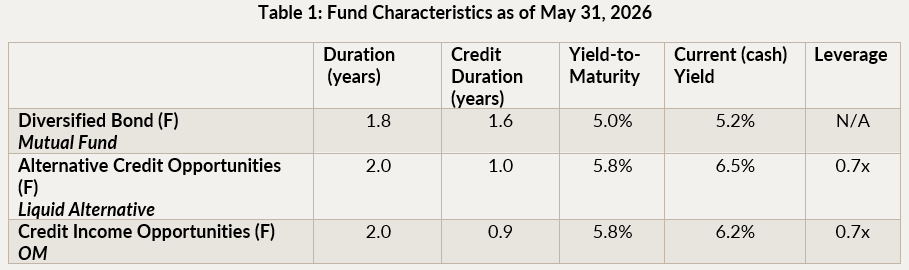

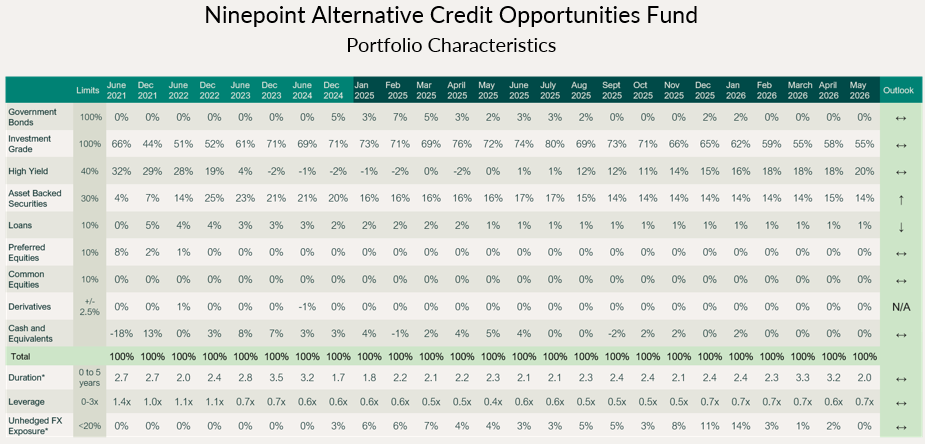

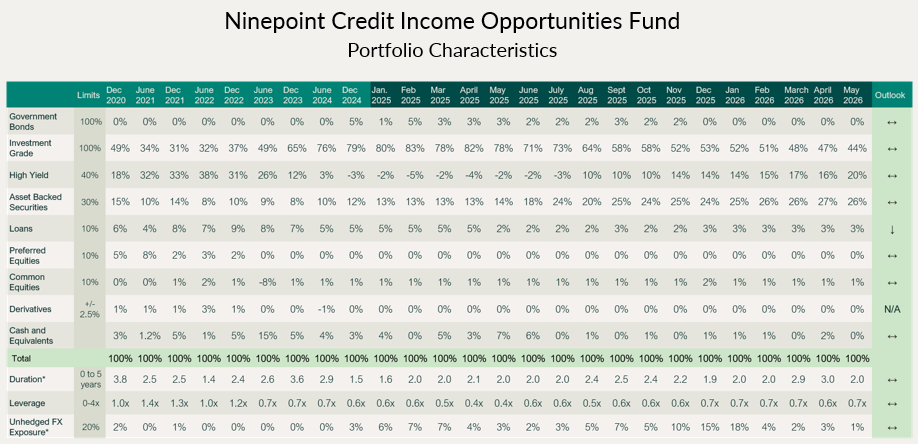

Table 1 below shows the various statistics and exposures as of month end. Our duration is at a comfortable 2 years, while spread/credit duration remained very low, due to the impact of credit hedges. Leverage went up in our alternative strategies (0.7x vs 0.6x last month), but was offset by upsizing credit hedges (low cost CDX collars). Given how cheap credit hedges are right now, this seems like a good way to maximize income while keeping a very defensive posture.

Click for larger image

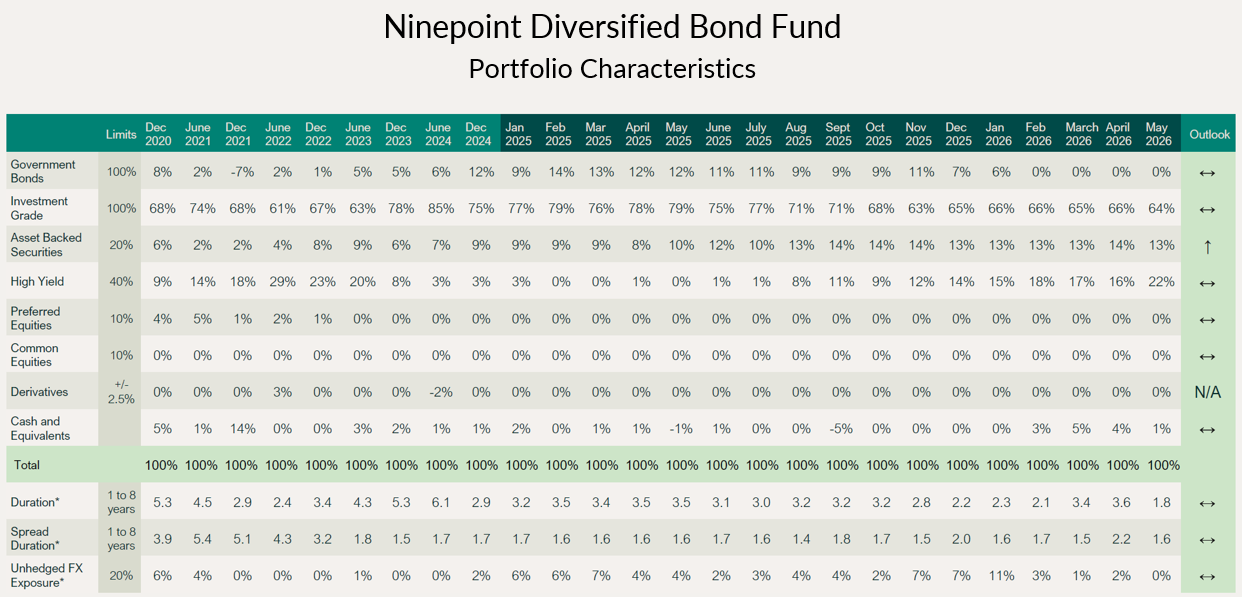

Ninepoint Diversified Bond Fund

NINEPOINT DIVERSIFIED BOND FUND - COMPOUNDED RETURNS¹ AS OF MAY 31, 2026 (SERIES F NPP118) | INCEPTION DATE: AUGUST 5, 2010

1M |

YTD |

3M |

6M |

1YR |

3YR |

5YR |

10YR |

15YR |

Inception |

|

|---|---|---|---|---|---|---|---|---|---|---|

Fund |

0.16% |

1.14% |

-0.01% |

0.99% |

3.64% |

5.82% |

1.81% |

2.86% |

3.16% |

3.55% |

Click for larger image

Ninepoint Alternative Credit Opportunities Fund

NINEPOINT ALTERNATIVE CREDIT OPPORTUNITIES FUND - COMPOUNDED RETURNS¹ AS OF MAY 31, 2026 (SERIES F NPP931) | INCEPTION DATE: APRIL 30, 2021

1M |

YTD |

3M |

6M |

1YR |

3YR |

5YR |

Inception |

|

|---|---|---|---|---|---|---|---|---|

Fund |

0.52% |

1.44% |

0.08% |

1.37% |

4.53% |

7.05% |

2.88% |

2.93% |

Click for larger image

Ninepoint Credit Income Opportunities Fund

NINEPOINT CREDIT INCOME OPPORTUNITIES FUND - COMPOUNDED RETURNS¹ AS OF MAY 31, 2026 (SERIES F NPP507) | INCEPTION DATE: JULY 1, 2015

1M |

YTD |

3M |

6M |

1YR |

3YR |

5YR |

10YR |

Inception |

|

|---|---|---|---|---|---|---|---|---|---|

Fund |

0.30% |

1.15% |

0.01% |

1.32% |

4.40% |

6.86% |

3.61% |

5.22% |

4.88% |

Click for larger image

Conclusion

Despite all the volatility, the portfolios have behaved well. As the potential range of economic outcomes continues to be wide, we intend to manage rate and credit risks tightly. We believe our current portfolio positioning is appropriate, but as always, we are ready to adjust our positioning, should things change materially.

Good luck and until next month.

Mark, Etienne & Nick

As always, please feel free to reach out to your product specialist if you have any questions.