|

|

|

|

(7 Day Change as of September 5, 2025 11:50AM ET)

|

Bitcoin Price: $110,828

2.22%

|

|

DeFi Total-Value-Locked: $155B

(1.90%)

|

Ethereum Price: $4,289

(1.01%)

|

|

Crypto Market Cap: $3.81T

(2.31%)

|

Bitcoin Range: $107,310 - $113,124

|

|

TKN.U Close: $20.06 (as at Sep 4, 2025)

|

Ethereum Range: $4,252 - $4,491

|

|

|

Bitcoin Dominance: 58.00%

0.69%

|

|

|

|

|

|

|

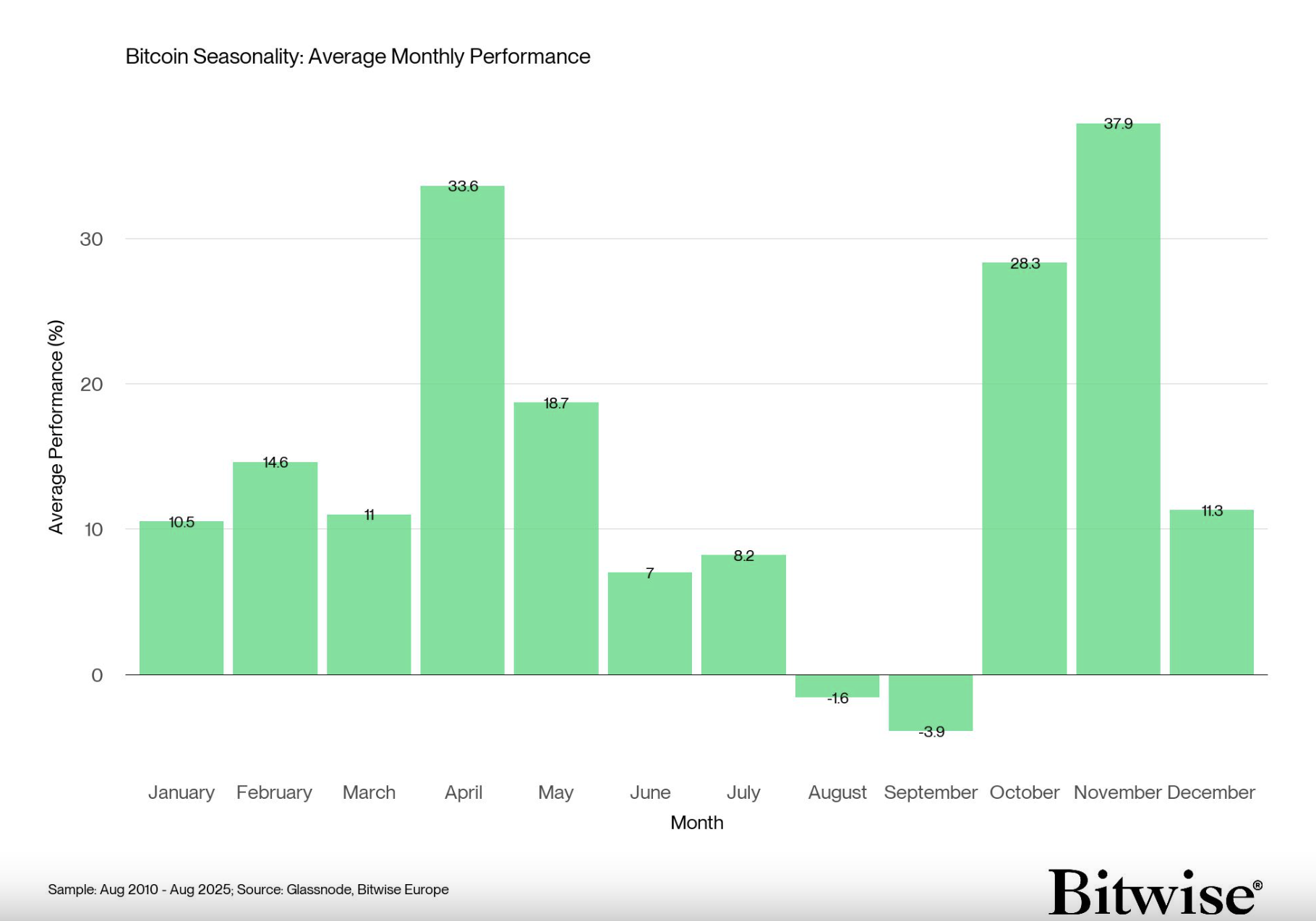

Does Seasonality Still Matter in Crypto?

|

Cryptoassets are highly reflexive: market perception regularly influences prices, thus changing perceptions. This cuts both ways. When the market thinks an event will have a positive impact on the price, such as the Bitcoin halvening, when the Bitcoin block reward get halved, prices typically follow. To wit, at the last halvening in April 2024, the price of Bitcoin was $64,000. Since then, it has risen by 70%. Every single halvening event has been followed by a sharp move upward.

As the price of Bitcoin goes up, it induces more people to buy in. The last halvening timed up perfectly with the launch of ETFs in the U.S., giving investors a convenient way to play the trade. People on X.com joke and debate about whether the 'halvening is priced in,' but buying BTC on the halvening has been a winning strategy.

Reflexivity cuts the other way too. One area where this plays out is with the concept of seasonality. Crypto investors did not invent the concept that asset prices behave differently depending on the month/season etc. In traditional finance, every spring you hear the cliche "Sell in May and Go Away." Never mind that there is

zero evidence that this is a good strategy, it still gets trotted out. I have always been pretty skeptical of seasonality, just as I am skeptical of horoscopes. Mercury is in retrograde, sell your NVIDIA! Huh?

But with crypto, I am more sympathetic, given the highly reflexive nature of the market and the (borderline irrational) faith that investors put on these heuristics and assumptions.

Our friends at Bitwise put together a helpful research report that touched on seasonality, highlighting the point with this chart:

Source: Bitwise Weekly Crypto Market Compass

So, is 'Downtember' (sorry I don't come up with these names), an inevitability? Should we all heed Greenday's advice and ask "wake me up when September ends?"

Though I loathe this expression, it's probably true that

t

his time is different. Markets have been consolidating all summer long. Rate cuts are coming soon. Fund flows into ETFs and DATs remain strong, with crypto ETFs

experiencing $35 billion of YTD net inflows and DATs

eclipsing $15 billion in fundraising in that same period, and in the next few weeks, we'll

likely get clarity on a Solana ETF. A wave of crypto companies has gone public with more coming. This broadening investment universe will likely draw in new buyers. September is back to school month. So sharpen your pencils and don't doze off.

|

|

THIS WEEK ON DEFI DECODED

|

|

|

|

|

|

Join Alex Tapscott as he decodes the world of crypto with special guest Jim Hiltner, Co-Founder and Head of Business Development at Superstate. Listen in as they discuss the accelerating adoption of tokenized real-world assets by issuers and investors worldwide, the Superstate origin story and its evolution, how tokenization democratizes access to U.S. dollar investment accounts, Superstate’s USTB and USCC onchain investment funds, its Opening Bell platform that enables public companies to tokenize their shares and why it stands out from other market offerings, Galaxy Digital’s move to tokenize its GLXY shares on Solana using Opening Bell this past week, the future of capital markets and the role of blockchains in reshaping access to capital and financial infrastructure, how Superstate evaluates which networks to issue assets on, and more.

|

|

|

|

By: Jake Moodie

, Analyst, Digital Asset Group at Ninepoint Partners

Tokenization Tipping Point 2.0: The March of Real-World Assets Coming Onchain Accelerates…

- Galaxy Digital teamed up with Superstate to let stockholders tokenize and hold GLXY shares on Solana. Using Superstate’s Opening Bell platform, this was the first time a public company tokenized its SEC-registered equity directly on a major blockchain.

- Ondo Finance launched Ondo Global Markets, a tokenized equity platform built on Ethereum. At first, it gives non-U.S. investors access to more than 100 U.S. stocks and ETFs onchain, with plans to expand to 1,000 by year-end and add support for Solana and BNB Chain.

- The tokenized gold market, driven mainly by Tether’s XAUT and Paxos’ PAXG, hit a new all-time high of about $2.6 billion.

- Citi released a report titled Securities Services Evolution, projecting that by 2030, 10% of market turnover could take place through tokenized assets. The key driver behind that forecast? Crypto’s first real killer app: tokenized dollars, or stablecoins. Specifically, Citi mentioned “bank-issued stablecoins.”

- All this comes just weeks after Anthony Scaramucci’s SkyBridge Capital announced it would tokenize $300 million of assets from two of its hedge fund strategies on Avalanche.

- And it follows a busy early July, when Robinhood launched tokenized Stock Tokens on Arbitrum, Kraken (via Backed) introduced tokenized xStocks on Solana, Gemini listed its first tokenized stock leveraging Dinari, and Coinbase’s Chief Legal Officer called tokenized equities a “huge priority.”

The bottom line: as we’ve been saying for years, the tokenization of every type of financial asset is already underway and speeding up. But not all tokenized assets are created equal. Structures vary widely across issuers, and some of the offerings above have drawn criticism for being synthetic or wrapped products rather than being natively issued by the underlying company. For a deeper dive on the differences, and to hear from a team that’s getting it right, check out this week’s

DeFi Decoded episode with Jim Hiltner, Co-Founder and Head of Business Development at Superstate.

Solana Looks Primed to be The Next Big Beneficiary of The DAT and ETF Wave. The Market May Already be Taking Notice.

Considering the impact DATs and ETFs have had on Bitcoin and Ethereum, it’s natural to ask which cryptoasset could be next to see a similar demand shock. A few weeks ago, we

shared a chart showing that Bitcoin DATs and ETFs had absorbed 7x more supply than was issued YTD, while Ethereum’s figure was an incredible 27x. So, what’s next? We think it’s Solana. There are two big reasons. First, late-August reports highlighted three large Solana-focused DATs in the works:

Sharps Technology with a $400M PIPE,

Pantera Capital’s Solana Co. targeting $1.25B, and a

Galaxy Digital/Multicoin/Jump consortium looking to raise $1B. Second, U.S. Solana ETFs could be only weeks away, with the SEC’s final deadline set for October 10, 2025, though approval could even come sooner. Ethereum showed us the playbook. The launch of its DATs kicked off a flywheel, pulling billions into ETFs and driving a strong rally, right when sentiment was at its lowest. Solana is in a different, but similar, spot today. After its historic 2024 run, it’s cooled off, lost its spotlight to Ethereum, and has been consolidating quietly for months. Now, with massive DATs preparing to launch and ETFs likely around the corner, the setup looks increasingly strong. If history rhymes, Solana has all the ingredients to be the next big winner of the DAT and ETF wave. Interestingly, since the last week of August, Solana is up 5% versus Bitcoin’s -1% and Ethereum’s -7%. Maybe the market is already catching on.

|

|

|

|

|

|

|

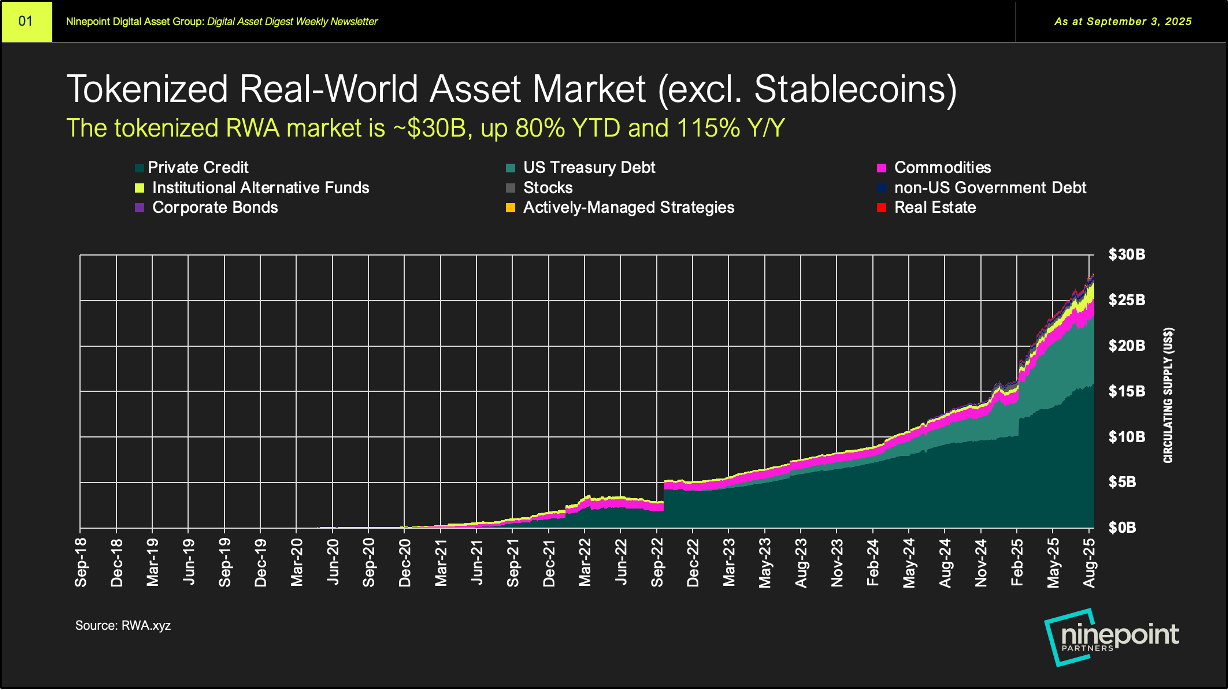

Chart 1:

Tokenized RWA Market is Nearly $30B Large, Growing More Than 2x in the Past Year

|

Given this past week’s tokenization-heavy theme, we wanted to take a look at the current state of the tokenized RWA market. Excluding stablecoins, the market is

now close to $30 billion, up an incredible 80% YTD and 115% Y/Y. The largest asset class is private credit, which makes up just over half of the market. The main issuer here is Figure. Founded in 2018 by SoFi co-founder Mike Cagney, Figure is a California-based fintech platform that uses blockchain to originate, fund, and trade loans. Its flagship product is a home equity line of credit, and to date the company

has originated more than $17 billion in loans across 200,000 homes. Like Gemini, Figure has recently filed a

Form S-1 to list on the Nasdaq under the ticker FIGR. It’s targeting a post-IPO valuation of roughly $4.3–$4.6 billion, which would raise about $526 million in gross proceeds at the high end of the range. The next two largest tokenized asset classes by AUM are U.S. Treasuries and commodities. Altogether, there are just over 270 issuers of tokenized products and 375,000 holders of these tokenized RWA products. While Figure’s assets are hosted on its own Provenance Blockchain, most of the rest of the market is based on Ethereum (53%) and ZkSync Era (15%), with the remaining spread across several other networks. And with the U.S. SEC recently launching

Project Crypto to bring financial markets onchain, we think the growth of this market will be explosive in the years to come.

|

|

|

|

|

|

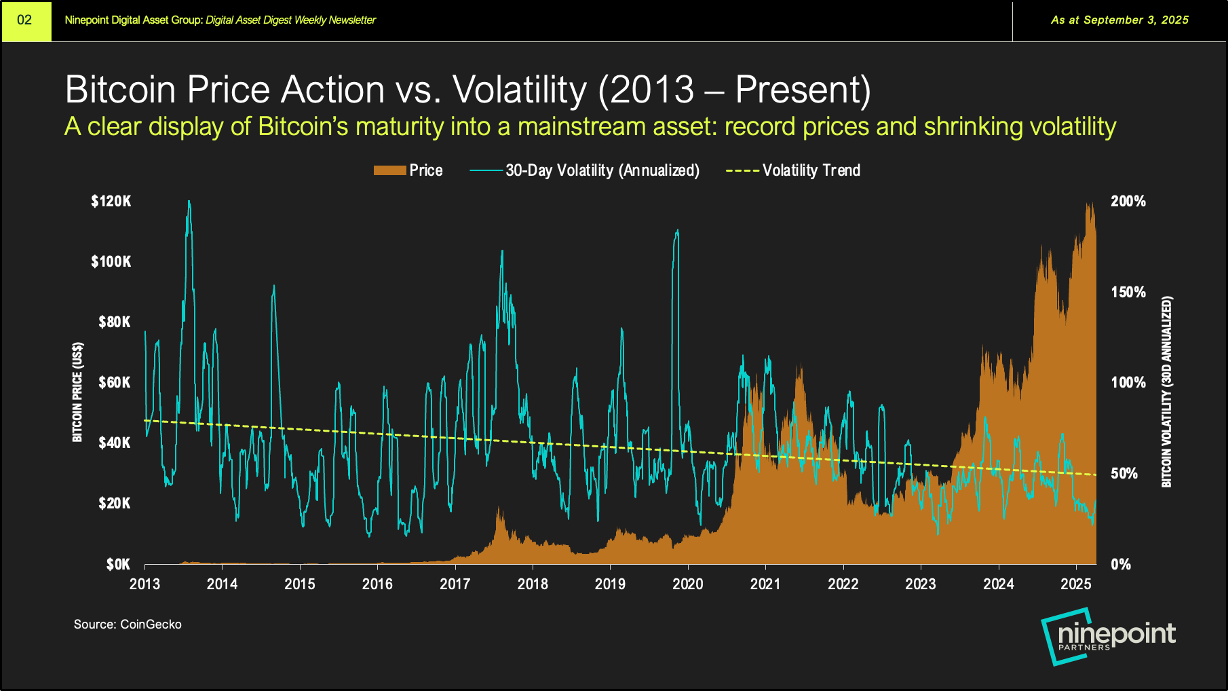

Chart 2:

Extreme Bitcoin Volatility is Breaking Down, Institutional Allocation Anchors Market

|

One of the most common critiques of Bitcoin from traditional investors is that it’s plagued by extreme volatility. We wanted to dig into this to separate fact from fiction. Looking at the chart, over the past decade, Bitcoin’s price has trended up and to the right, setting new highs, while its volatility has come down dramatically. That said, Bitcoin is still more volatile than traditional assets: its 30-day annualized volatility sits around

35%, compared to

10.6% for the S&P 500 and

12.6% for gold. Still, as the trend line shows, Bitcoin’s volatility has dropped massively and is now sitting at multi-year lows. So what does this all mean? For emerging markets, especially in tech, high volatility is normal early on as excitement drives big rallies and big sell-offs. Past crypto cycles were mostly retail-driven, which led to wild booms and busts. But this cycle looks different. Put simply, crypto’s boom-bust cycles may be fading. Regulation is reducing blow-up risk, enterprise adoption is strengthening network effects, and institutional capital is anchoring the market. The asset class is maturing in all the right ways. In fact, Bitcoin’s historically low volatility was highlighted in a JPMorgan

research note last week. The analysts looked at Bitcoin’s historical volatility to gold’s and concluded that, on a volatility-adjusted basis, Bitcoin’s fair value could reach about $126,000 by year-end.

|

|

|

September 5, 2025

September 5, 2025