|

|

|

|

(7 Day Change as of September 12, 2025 2:40PM ET)

|

Bitcoin Price: $116,507

4.76%

|

|

DeFi Total-Value-Locked: $162B

4.52%

|

Ethereum Price: $4,627

7.47%

|

|

Crypto Market Cap: $4.06T

6.56%

|

Bitcoin Range: $110,064 - $116,509

|

|

TKN.U Close: $21.39 (as at Sep 12, 2025)

|

Ethereum Range: $4,248 - $4,627

|

|

|

Bitcoin Dominance: 57.10%

(1.55%)

|

|

|

|

|

|

|

The Sun Also Rises: Why SOL is Ascendent

|

A few weeks ago we asked readers "

are you ready for a long Alt Szn?" highlighting how Bitcoin's long reign as the top performing cryptoasset was showing signs of exhaustion, and that Ethereum and other assets could soon be ascendant.

Since we wrote that note, Ethereum has outperformed Bitcoin

by 33%. Incidentally, this has helped contribute to significant outperformance for our Crypto and AI Leaders ETF (TKN-TSX), which has been overweight ETH, and is

up over 7% since that note, compared with Bitcoin down 2.3%.

We got the ETH call right, but it's still TBD for the rest of the cryptoasset space. That’s because this market is playing out somewhat differently than past cycles. Instead of a "rising tide lifts all/most boats," we now have a "rising tide allows one boat at a time out of dry dock before the tide recedes and we have to wait a while for the next one" (I will work on this metaphor - or maybe ask Chat GPT).

We've long held Solana is overdue for a rally. In last week's note we

wrote: “Solana looks primed to be the next big beneficiary of the digital asset treasuries (DATs) & ETF wave" A huge influx of capital from DATs and ETFs, all else being equal, could drive the price higher.

Our thesis was pretty simple. Bitcoin ETFs and popular DATs like MicroStrategy (MSTR) and more recently the ETH DATs like Bitmine (BMNR) helped put a strong bid under ETH and BTC. Since the Bitcoin ETFs launched in January of 2024, Bitcoin is

up over 150%. Since Bitmine converted to an ETH DAT, Ethereum

is up over 90%.

ETH Bulls were keen to point out that between the DATs and ETFs, net buying

was 27x as high as the net new supply.

Our one-week call was right. Solana is up around 20% while Bitcoin is up 4% and ETH up 6%. Will it continue? Currently, SOL DATs

represent only $1.5 billion out of the total $115 billion market capitalization of DATs, and SOL DATs hold 1.06% of total SOL supply, compared to BTC DATs (3.5%) and ETH DATs (3.1%). So there’s room to catch up.

Yesterday, Solana got a jolt after Galaxy

announced that its Solana DAT had raised $1.65 billion, more than target, and doubling the size of the SOL DAT market overnight. We hear many more are coming. That augurs well for the would-be Ethereum competitor.

Tom Lee, Chairman of Bitmine has been on TV telling viewers that Ethereum is the blockchain for stablecoins and tokenized real-world assets (RWAs). That's mostly true (or at least it has been historically): today

around 63% of stablecoin market, equivalent to $175 billion, is hosted on the Ethereum network or its L2s. But it has been steadily losing market share to Solana and others.

Tom Lee is Ethereum’s Promoter-in-Chief. Could anyone sound more bullish or more skilfully pump their bags? Enter Galaxy’s Mike Novogratz, who said “hold my beer,” getting on

CNBC yesterday morning to make his case:

“Why Solana at this moment? The total transactions per second that Solana can do in a day is 14 billion. That's more than total transactions on equities, fixed income, commodities and foreign exchange. So, you’ve got a blockchain that’s fast enough, tailor made to be the blockchain for financial markets. And you’ve got an SEC chair who’s saying I want you to build onchain.”

Novogratz was saying that Solana’s theoretical limit is 14 billion transactions a day - that it can handle the transaction volumes of major financial markets like stocks and bonds, and that it’s probably inevitable that more assets move onchain, especially with the regulatory all-clear. I agree with all of that. I also think someone watching this could read it as the Solana network is

already doing 14 billion transactions a day, making it a more active market than those other ones - combined!

Anyway, if that’s what we can come to expect from Mr. Novogratz, he may give Tom Lee a run for his money. Probably, both ETH and SOL holders benefit here. One must wonder if other blockchain networks have their own skilful spokespeople to translate their message to the mainstream. That, more than anything, could be the leading indicator of who’s next.

|

|

THIS WEEK ON DEFI DECODED

|

|

|

|

|

|

Join Alex Tapscott and Andrew Young as they decode the world of crypto. Listen in as they discuss the accelerating convergence of crypto and Wall Street, the big opportunities and implementation challenges with onchain finance, Solana’s outsized rally following large SOL DAT announcements with ETFs on the horizon, a few of the inefficiencies that still exist in today’s crypto market, the widening disconnect between all-time high prices and deteriorating sentiment, whether looming rate cuts could meaningfully move the market, and more.

|

|

|

|

By: Jake Moodie

, Analyst, Digital Asset Group at Ninepoint Partners

Nasdaq Puts Tokenized Equities on the Table While CBOE Plans Bitcoin and Ethereum Perps

Following our tokenization-themed

Digital Asset Digest last week, Nasdaq

filed a proposal with the SEC on Monday to allow tokenized stocks and ETFs to trade alongside their traditional counterparts. If approved, investors could choose to settle trades conventionally or onchain, with tokenized shares carrying the same rights as the underlying securities, including voting, dividends, and liquidation claims. To stay consistent with existing market infrastructure, these tokenized assets would still be cleared through the Depository Trust Company. This marks the first major step toward embedding blockchain-based settlement into the heart of U.S. equity markets, potentially as early as next year, as Washington sharpens its focus on market-structure reform and tokenization standards. Then, just one day following, CBOE

announced that it’s set to launch ‘continuous futures’ for Bitcoin and Ethereum on November 10, pending regulatory approval. For crypto-native individuals, that term may sounds awfully familiar. And that’s because it is. These are perpetual futures, or perps, which are futures contracts with no expiry date. They allow traders to take on continuous leveraged positions tied to price movements, without ever having to settle or take delivery of the underlying cryptoassets. According to the report, CBOE said these will “give both institutional and retail traders a safer way to make long-term wagers on crypto” and be cleared through its own U.S.-regulated clearinghouse. As we’ve said time and time again, the line between crypto and traditional finance is increasingly blurring, and these headlines are driving the point home.

The Hyperliquid Stablecoin Battle Heats Up, Turning Circle’s Yield into Massive Ecosystem Opportunity

Hyperliquid, the leading decentralized perpetuals exchange, announced last week that

it’s auctioning off its native USDH stablecoin ticker via a governance vote. This sparked a swift wave of proposals from multiple issuers, with Hyperliquid validators set to vote on their preferred option on September 14. This is a big moment for the exchange because right now it holds around $5.5 billion of USDC, about 7.5% of all supply. At a 4% yield, that’s roughly $220 million in annual revenue for Circle, none of which flows back to the Hyperliquid ecosystem. By activating USDH, the goal is to capture some of that value and redirect it into the ecosystem, turning what has been an outflow into a native profit stream. A broad slate of issuers, including Paxos, Ethena, Frax Finance, Native Systems, and others, have thrown their hats in the ring, submitting proposals that highlight revenue-share terms, design models, reserve backing, differentiators, and the scale and experience they bring to win the mandate. Though the final outcome hinges on the upcoming vote, Polymarket odds currently have Native Markets as the clear frontrunner at 96%, with Paxos (4%) trailing behind. The bigger picture here is that Hyperliquid has flipped the usual stablecoin playbook. In the past, exchanges created and controlled their own stablecoins: Bitfinex with Tether, Coinbase with USDC. This time, the exchange isn’t the issuer but instead gets to choose one, forcing some of the biggest names in both DeFi and TradFi to compete for access. With billions in stablecoin float on the line and hundreds of millions in potential annual revenue, this outcome is being closely watched.

|

|

|

|

|

|

|

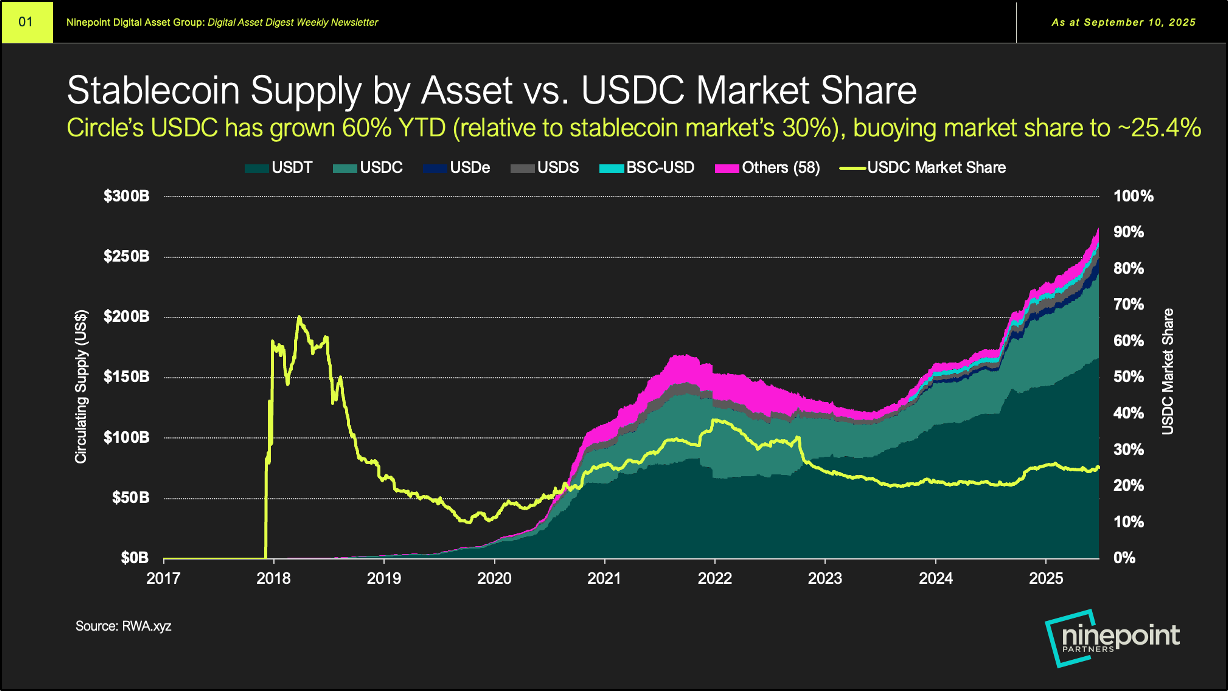

Chart 1:

Circle’s $70B USDC Stablecoin’s Momentum in Focus as Bulls & Bears Weigh In

|

Following the Hyperliquid USDH stablecoin announcement this past week, it’s worth revisiting Circle’s USDC and its position in the market. USDC supply

currently sits at $70 billion, up 70% YTD, more than double the 30% growth of the broader stablecoin market and well ahead of Tether’s 21%. This surge has lifted USDC’s market share from 21.4% at the start of the year to 25.4% today. We see two main drivers behind this growth. First, Circle’s IPO in May gave the company the credibility and transparency of a U.S.-listed public entity, a clear advantage over private competitors. Second, the GENIUS Act, signed into law by President Trump in July, established the first comprehensive U.S. stablecoin framework. Because Circle is domiciled in the U.S. as a public company, it is uniquely positioned to benefit from this regulation, giving it an edge over overseas issuers that lack the same standing. Still, the competitive landscape is intensifying as both crypto-native players and large traditional financial institutions move in, making every stablecoin dollar more valuable than ever. The Hyperliquid development underscores this reality: about $5.5 billion of USDC, roughly 7.5% of supply, is currently used as collateral on its perpetuals platform. With Hyperliquid preparing to roll out its own stablecoin, some of that demand for USDC could be displaced. If all $5.5 billion were redeemed, and assuming Circle earns a 4% yield on the treasuries backing USDC, the potential revenue impact could reach $220 million, a worst-case scenario, but meaningful nonetheless. But as Needham recently pointed out, there are also strong reasons for optimism. USDC balances on Binance have climbed to $9.1 billion as of the end of August, showing robust M/M growth. In addition,

new CFTC guidance allows U.S. customers to access foreign exchanges like Binance. Given Binance and Circle’s strategic partnership, this could be a huge growth engine for USDC supply and thus Circle’s economics. Ultimately, competition should be viewed as a long-term positive. It forces issuers to innovate, differentiate, and deliver better offerings, a process that benefits end users and ensures stablecoins continue evolving.

|

|

|

|

|

|

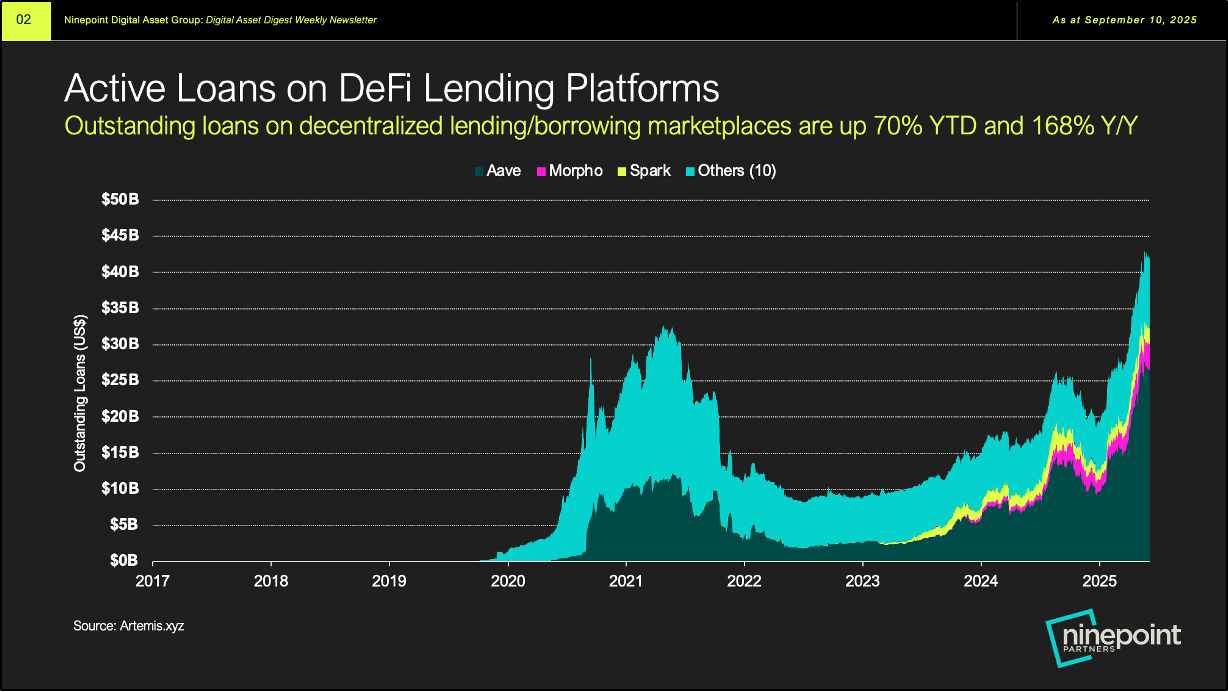

Chart 2:

DeFi Lending Platforms Hit Record Highs: >$100B Deposits & $42B of Active Loans

|

One of the most overlooked yet fastest-growing sectors in crypto right now is DeFi lending. The best way to think of these platforms is like traditional lending marketplaces where people can borrow and lend assets, but instead of bankers and brokers, everything runs on automated smart contracts. This enables true peer-to-peer lending, open to anyone worldwide with an internet connection, without the costs and delays of intermediaries. Today, total active loans on DeFi lending platforms

stand at an all-time high of $42 billion, more than double the $20 billion peak from the last cycle in 2021, and up 70% YTD and roughly 170% over the past year. And it’s not just borrower demand that’s booming; deposits on these platforms just

surpassed $100 billion for the first time in history. Take Aave, the largest and one of the longest-running DeFi lenders: it

holds $64 billion in deposits. That alone would rank it the 39th largest U.S. commercial bank. On top of that, Aave is one of the most profitable apps in the crypto, ecosystem, generating over $80 million in revenue and $33 million in earnings YTD, all with fewer than 100 employees. Like we

said of Tether a few weeks ago, Aave also raises the question: is this an outlier or proof of a new kind of blockchain-native business that can scale globally with software instead of manpower? Zooming out, with the U.S. administration leaning deeper into crypto, from the SEC’s “Project Crypto” to bring capital markets onchain, to the surge in tokenized equity offerings, to the rising share of decentralized exchange volume against centralized exchanges, it’s hard to imagine DeFi lending platforms not being one of the biggest winners as more assets move onto these rails.

|

|

|

September 12, 2025

September 12, 2025