Ninepoint Flow-Through Update

Q3 2023 Commentary

Ninepoint 2022 Flow-Through Update

The Net Asset Value (NAV) for the Ninepoint 2022 FTLP Fund- Series A on September 30, 2023 was $7.93/unit.

The fund exited the quarter weighted as follows: 73% precious metals, 15% base metals, 7% uranium, and 5% energy. Precious metal equities have dramatically underperformed gold bullion. From its peak in 2022, the inception year of the 2022 Flow-Through fund, the VanEck Junior Gold Miners ETF has fallen 37%. Over the same period, gold bullion has returned 1%. Entering 2023, I decided to maintain the majority of the portfolio as initially constructed, specifically the exposure to gold equities. The outlook for gold bullion was constructive and small capitalization gold equities sold off dramatically into year-end 2022 as tax loss selling took hold, dramatically underperforming bullion. As of writing, gold bullion is up 8.4% year-to-date. But despite gold bullion’s positive performance, the 2022 FTLP is down 40% year-to-date. Why? Quite simply, this is the worst environment for small capitalization mining equities, specifically gold equities, I have seen in my 20+ year career. Below you will find a chart that details the stock price performance of several serial flow-through issuers.

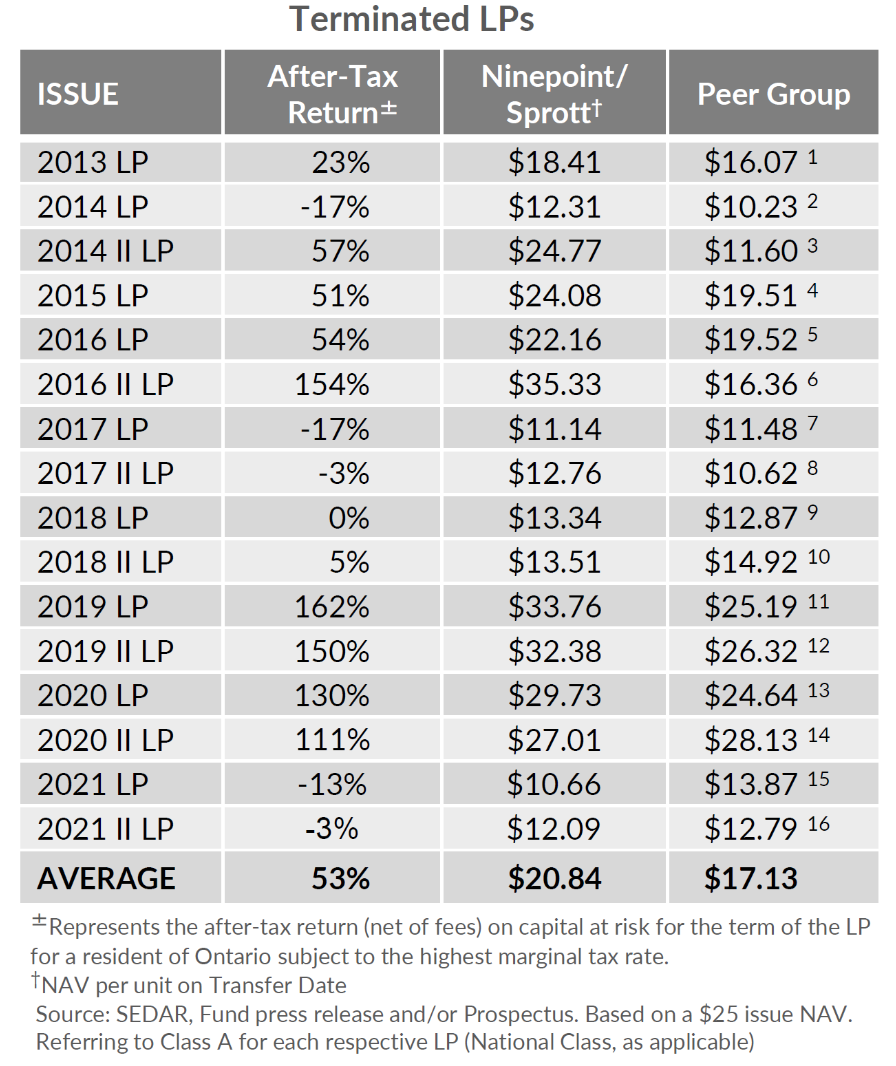

We have always stressed to clients that commodities and resource equities are incredibly volatile. The performance of the flow-through funds will range from spectacular to awful. After two years of posting double-digit after-tax returns in the 2019 and 2020 flow-through limited partnerships, the small-cap resource trade has had a difficult stretch. I would like to remind investors of the flow-through track record and the need to evaluate returns on an after-tax basis. I would also like to remind clients of the importance of remaining committed to the flow-through strategy during poorly performing periods because the product track record clearly illustrates the benefit of consistent participation, particularly following poor-performing issues.

Investors are routinely fixated on pre-tax returns. This is surprising since most investors rarely capture those returns on an after-tax basis as most investors are taxed on capital gains and income. When evaluating the returns of a flow-through fund the only meaningful measure of performance is on an after-tax basis considering it is a tax-mitigating product. Although after-tax return figures are not calculated until the fund is terminated, investors should consider some of the following points when gauging how the investment is performing on an after-tax basis. Many investors incorrectly evaluate the performance of the fund based on the initial investment of $25/unit thereby not accounting for any of the tax benefits.

It is also important to remember the $25/unit is not adjusted for initial fees, premiums paid to acquire flow-through shares or tax benefits. Most importantly, it is critical that investors understand how impactful the tax benefits are to the per-unit economics. As disclosed in the 2022 Flow-Through LP prospectus, the breakeven point on an after-tax basis for an Ontario investor taxed at the highest marginal rate is approximately $12.30/unit. The breakeven NAV for a flow-through fund is the after-tax breakeven point, not the $25/unit initial offering price. Investors need to understand this to correctly evaluate the performance of any flow-through fund.

Ninepoint 2022 Short Duration Flow-Through Update

The Net Asset Value (NAV) for the Ninepoint 2022 Short Duration Fund- Series A on September 30, 2023 was $13.93/unit.

The fund exited the quarter weighted as follows: 59% precious metals, 19% base metals and 22% uranium. Precious metal equities have dramatically underperformed gold bullion. From its peak in 2022, the inception year of the 2022 Flow-Through fund, the VanEck Junior Gold Miners ETF has fallen 37%. Over the same period, gold bullion has returned 1%. Entering 2023, I decided to maintain the majority of the portfolio as initially constructed, specifically the exposure to gold equities. The outlook for gold bullion was constructive and small capitalization gold equities sold off dramatically into year-end 2022 as tax loss selling took hold, dramatically underperforming bullion. As of writing, gold bullion is up 8.4% year-to-date. But despite gold bullion’s positive performance, the 2022 Short Duration FTLP is down 27% year-to-date. Why? Quite simply, this is the worst environment for small capitalization mining equities, specifically gold equities, I have seen in my 20+ year career. Below you will find a chart that details the stock price performance of several serial flow-through issuers.

The 2022 Short Duration FTLP (SD) has outperformed the 2022 FTLP because of several factors. The SD proceeds were deployed later in the year following a significant correction in resource equities. The SD had greater exposure to uranium equities, which outperformed other resource equities. Finally, the SD had a large position that was acquired at a significant premium.

We have always stressed to clients that commodities and resource equities are incredibly volatile. The performance of the flow-through funds will range from spectacular to awful. After two years of posting double-digit after-tax returns in the 2019 and 2020 flow-through limited partnerships, the small-cap resource trade has had a difficult stretch. I would like to remind investors of the flow-through track record and the need to evaluate returns on an after-tax basis. I would also like to remind clients of the importance of remaining committed to the flow-through strategy during poorly performing periods because the product track record clearly illustrates the benefit of consistent participation, particularly following poor-performing issues.

Investors are routinely fixated on pre-tax returns. This is surprising since most investors rarely capture those returns on an after-tax basis as most investors are taxed on capital gains and income. When evaluating the returns of a flow-through fund the only meaningful measure of performance is on an after-tax basis considering it is a tax-mitigating product. Although after-tax return figures are not calculated until the fund is terminated, investors should consider some of the following points when gauging how the investment is performing on an after-tax basis. Many investors incorrectly evaluate the performance of the fund based on the initial investment of $25/unit thereby not accounting for any of the tax benefits.

It is also important to remember the $25/unit is not adjusted for initial fees, premiums paid to acquire flow-through shares or tax benefits. Most importantly, it is critical that investors understand how impactful the tax benefits are to the per-unit economics. As disclosed in the 2023 Short Duration Flow-Through LP prospectus, the breakeven point on an after-tax basis for an Ontario investor taxed at the highest marginal rate is approximately $12.30/unit. Note that this breakeven figure does not account for the Critical Mineral Exploration Tax Credit. The breakeven NAV for a flow-through fund is the after-tax breakeven point, not the $25/unit initial offering price. Investors need to understand this to correctly evaluate the performance of any flow-through fund

Ninepoint 2023 Flow-Through Update

The Net Asset Value (NAV) for the Ninepoint 2023 FTLP- Series A on September 30, 2023 was $16.29/unit.

The fund raised $33M in April. As of September 30, 2023, 92% of the initial proceeds had been either invested or committed. 62% had been allocated to gold mining equities, 13% to uranium equities, and 9% to base metal equities while other metals account for the balance. The portfolio currently consists of 29 companies with a weighted average market capitalization of $100M. The weighted average premium paid was 5%.

As disclosed in the 2023 Flow-Through LP prospectus, the breakeven NAV on an after-tax basis for an Ontario investor taxed at the highest marginal rate is approximately $12.25/unit. Note that this breakeven figure does not account for the Critical Mineral Exploration Tax Credit. The breakeven NAV for a flow-through fund is the after-tax breakeven point, not the $25/unit initial offering price. Investors need to understand this to correctly evaluate the performance.

Ninepoint Resource Fund

The fund exited the quarter weighted as follows: 50% oil and gas, 21% precious metals, 10% base metals and 18% uranium. Year-to-date the fund returned -2.0%. The fund is focused on small-cap resource equities. Oil and gas and uranium equities contributed to the fund’s performance while all other equities detracted from performance. Uranium prices were one of the few bright spots amongst commodities, surging approximately 25% and 46% in Q3/23 and YTD, respectively. Also noteworthy was the exceptionally poor performance of small-cap gold equities despite gold bullion’s positive performance. In fact, this is the worst environment for junior gold exploration equities I have seen in my 20+ year career.

Ninepoint Resource Fund Class

The fund exited the quarter weighted as follows: 59% precious metals, 21% uranium, 18% base metals, and 4% energy. Year-to-date the fund has returned -3.1%. The fund is focused on small-cap resource equities. Uranium equities contributed to the fund’s performance while all other equities detracted from performance.

Jason Mayer CFA, MBA

Sprott Asset Management

Sub-Advisor to the Fund

References

1. Peer Group includes: Middlefield, Frontstreet, NCE, Brompton, Maple Leaf, CMP

2. Peer Group includes: Middlefield, Frontstreet, NCE, Brompton, Maple Leaf, CMP, Canoe

3. Peer Group includes: Middlefield, Frontstreet, Maple Leaf

4. Peer Group includes: Middlefield, NCE, Brompton, Maple Leaf, CMP, Canoe

5. Peer Group includes: Middlefield, NCE, Maple Leaf, CMP, Canoe

6. Peer Group includes: Marquest, Maple Leaf

7. Peer Group includes: Middlefield, Brompton, Maple Leaf, CMP

8. Peer Group includes: Middlefield, Maple Leaf

9. Peer Group includes: Middlefield, Maple Leaf, CMP

10. Peer Group includes: Maple Leaf

11. Peer Group includes: Middlefield, CMP, Maple Leaf

12. Peer Group includes: Middlefield, Maple Leaf

13. Peer Group includes: Middlefield, CMP, Maple Leaf

14. Peer Group includes: Middlefield, Maple Leaf

15. Peer Group includes: Middlefield, CMP

16. Peer Group includes: Middlefield, Maple Leaf

Series A NAV Details ($) Per Unit as at September 30, 2023 (Before Tax)

| Fund Name | NAV (Series A) |

| Ninepoint 2022 Flow-Through LP - National | $7.93 |

| Ninepoint 2022 Flow-Through LP - Quebec | $8.16 |

| Ninepoint 2022 Short Duration Flow-Through LP | $13.93 |

| Ninepoint 2023 Flow-Through LP | $16.29 |

The Fund is generally exposed to the following risks. See the prospectus of the Fund for a description of these risks: concentration risk; credit risk; currency risk; cybersecurity risk; derivatives risk; exchange traded funds risk; foreign investment risk; inflation risk; interest rate risk; liquidity risk; market risk; regulatory risk; securities lending, repurchase and reverse repurchase transactions risk; series risk; short selling risk; small capitalization natural resource company risk; specific issuer risk; tax risk.

Ninepoint Partners LP is the investment manager to a number of funds (collectively, the “Funds”). Important information about these Funds, including their investment objectives and strategies, purchase options, and applicable management fees, performance fees (if any), and expenses, is contained in their prospectus. Please read the prospectus carefully before investing. Commissions, trailing commissions, management fees, performance fees, other charges and expenses all may be associated with investing in the Funds. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated. This communication does not constitute an offer to sell or solicitation to purchase securities of the Funds. The information contained herein does not constitute an offer or solicitation by anyone in the United States or in any other jurisdiction in which such an offer or solicitation is not authorized or to any person to whom it is unlawful to make such an offer or solicitation. Prospective investors who are not resident in Canada should contact their financial advisor to determine whether securities of the Fund may be lawfully sold in their jurisdiction.

The opinions, estimates and projections (“information”) contained within this report are solely those of Ninepoint Partners LP and are subject to change without notice. Ninepoint Partners makes every effort to ensure that the information has been derived from sources believed to be reliable and accurate. However, Ninepoint Partners assumes no responsibility for any losses or damages, whether direct or indirect, which arise out of the use of this information. Ninepoint Partners is not under any obligation to update or keep current the information contained herein. The information should not be regarded by recipients as a substitute for the exercise of their own judgment. Please contact your own personal advisor on your particular circumstances. Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any investment funds managed by Ninepoint Partners. Any reference to a particular company is for illustrative purposes only and should not to be considered as investment advice or a recommendation to buy or sell nor should it be considered as an indication of how the portfolio of any investment fund managed by Ninepoint Partners is or will be invested. Ninepoint Partners LP and/or its affiliates may collectively beneficially own/control 1% or more of any class of the equity securities of the issuers mentioned in this report. Ninepoint Partners LP and/or its affiliates may hold short position in any class of the equity securities of the issuers mentioned in this report. During the preceding 12 months, Ninepoint Partners LP and/or its affiliates may have received remuneration other than normal course investment advisory or trade execution services from the issuers mentioned in this report.

Ninepoint Partners LP: Toll Free: 1.866.299.9906. DEALER SERVICES: CIBC Mellon GSSC Record Keeping Services: Toll Free: 1.877.358.0540

Investment Team

Related Funds

Historical Commentary

Toronto, Ontario M5J 2J1 Canada