Why the timing of returns matters in retirement.

For many investors approaching retirement, the focus is often on a familiar set of questions:

“Am I saving enough?”

“Will my portfolio keep growing?”

“Can I afford the retirement lifestyle I want?”

But once retirement begins, another question can become just as important:

What happens if markets decline at the wrong time?

This is the challenge behind sequence of returns risk, one of the most important and often overlooked aspects of retirement income planning.

For advisors, it can also be a useful conversation starter with clients nearing retirement. As the focus shifts from building wealth to drawing income from a portfolio, the order of market returns can matter just as much as the average return over time.

Why Retirement Changes the Math

During an investor’s working years, market volatility can often be viewed as temporary. Contributions continue, time remains on their side, and market recoveries can help repair short-term declines.

Once withdrawals begin, that dynamic changes.

Negative returns early in retirement can have a lasting impact on a portfolio’s future earning potential. Even if markets recover later, the portfolio may not fully regain its previous trajectory because capital was already withdrawn during the downturn.

In other words, the issue is not simply how much markets decline. It is when those declines occur.

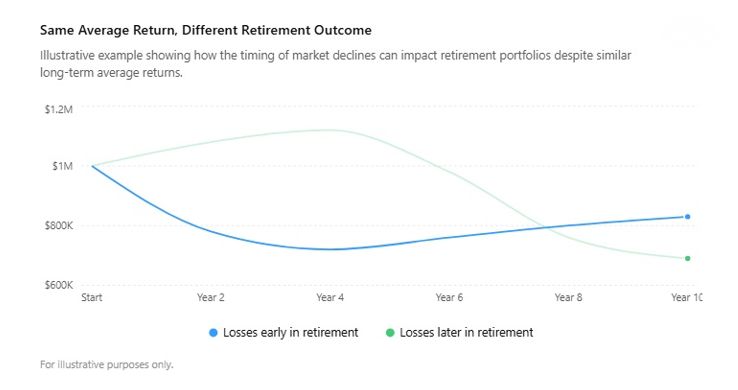

The Same Returns, Very Different Outcomes

Consider two retirees who each begin retirement with a $1 million portfolio and withdraw $50,000 annually.

Both earn the same average return over retirement. However, one experiences market losses early in retirement, while the other experiences those losses later.

When losses occur early, withdrawals may force the investor to sell assets when portfolio values are depressed. This reduces the amount of capital left to participate in future recoveries.

That is what makes sequence risk so powerful, and so difficult to understand intuitively. A portfolio can appear to have “recovered” years later, while the retiree’s financial position remains permanently weakened.

The damage often goes unnoticed.

2022: A Real-World Reminder

The events of 2022 served as an important reminder of this risk.

Both equities and bonds declined sharply in the same calendar year, challenging the assumption that traditional diversification will always cushion retirement portfolios during periods of stress.

For retirees drawing income, this created a particularly difficult environment. Portfolio values declined while withdrawals continued, and defensive assets provided less protection than many investors expected.

Importantly, this does not mean balanced portfolios “failed.” Rather, it reinforces that retirement income planning involves more than asset allocation alone. The transition from accumulation to decumulation introduces a different set of risks, behaviours, and planning considerations.

Accumulation and Decumulation Are Different

During accumulation, market declines can create future opportunity. Investors continue contributing, benefit from time and compounding, and may be able to wait for recoveries.

During retirement, withdrawals reverse the compounding process. Liquidity needs become immediate and unavoidable. The objective is no longer simply maximizing growth. It becomes balancing growth, income generation, capital preservation, and withdrawal sustainability over what may be a multi-decade retirement horizon.

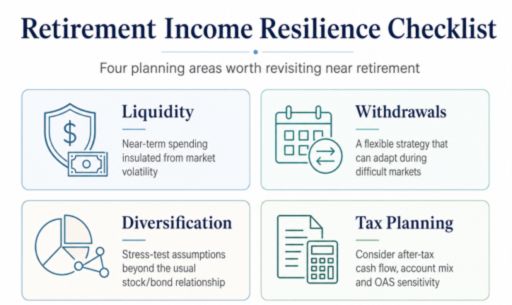

Planning Conversations Worth Revisiting

Sequence risk is not something that can necessarily be “solved” with a single product or allocation change. Instead, it can serve as a useful framework for more thoughtful retirement income planning conversations.

For clients nearing or entering retirement, several areas may be worth revisiting.

Liquidity and Near-Term Income Needs

How much of a retiree’s near-term spending should be insulated from market volatility?

Some retirement income plans include dedicated liquidity reserves or lower-volatility holdings that may help reduce the need to sell growth-oriented investments during periods of market stress. For clients entering retirement, even having several years of anticipated withdrawals set aside separately may help create flexibility during difficult markets.

Withdrawal Strategy

A static withdrawal rate may appear sustainable during strong markets but become more vulnerable after negative return periods, particularly early in retirement.

Questions worth considering include:

- Should withdrawals remain fixed every year?

- Is there room for spending flexibility during down markets?

- Are discretionary and non-discretionary expenses clearly separated?

- Could withdrawals be adjusted based on market conditions or portfolio performance?

Even modest flexibility can help improve long-term portfolio sustainability.

Retirement income planning also extends beyond withdrawal rates alone. The structure and tax characteristics of retirement income sources can materially affect after-tax cash flow and government benefit exposure.

For some retirees, considerations such as dividend income, capital gains treatment, registered versus non-registered withdrawals, and potential Old Age Security clawbacks may all play a role in building a more resilient retirement income plan.

Related reading: Not All Retirement Income Is Equal: Covered Call ETFs and the OAS Conversation

Portfolio Diversification During Stress Periods

Many investors think diversification simply means “stocks go down, bonds go up.”

For advisors and investors, this may be an opportunity to revisit how portfolios are expected to behave during periods of elevated inflation, rising rates, or broad market dislocations.

Stress-testing retirement income plans against different market environments may help uncover vulnerabilities that are not obvious during more stable periods.

Communication and Expectations

One of the more challenging aspects of sequence risk is that investors may not immediately recognize the damage.

A portfolio that eventually “recovers” can still leave a retirement plan on weaker footing if significant withdrawals occurred during the downturn. That makes proactive communication especially important near retirement and during the early retirement years.

Looking Beyond Average Returns

Sequence risk often remains invisible in traditional performance discussions.

Average returns, long-term market assumptions, and portfolio growth charts can all appear reasonable while masking the impact of poor early-retirement outcomes.

That is why retirement planning requires a broader lens. One that considers not just expected returns, but also withdrawal sequencing, investor behaviour, liquidity management, tax efficiency, and portfolio resilience during adverse environments.

For retirees, a market decline is not always just a temporary setback.

Sometimes the market recovers, but the retirement plan does not.

The opinions, estimates and projections (“information”) contained within this report are solely those of Ninepoint Partners LP (“Ninepoint”) and are subject to change without notice. Ninepoint makes every effort to ensure that the information has been derived from sources believed to be reliable and accurate. However, Ninepoint assumes no responsibility for any losses or damages, whether direct or indirect, which arise out of the use of this information. Ninepoint is not under any obligation to update or keep current the information contained herein. The information should not be regarded by recipients as a substitute for the exercise of their own judgment. Please contact your own personal advisor on your particular circumstances. Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any investment funds managed by Ninepoint Partners LP. These views are not to be considered as investment advice nor should they be considered a recommendation to buy or sell.

The information contained herein does not constitute an offer or solicitation by anyone in the United States or in any other jurisdiction in which such an offer or solicitation is not authorized or to any person to whom it is unlawful to make such an offer or solicitation. Prospective investors who are not resident in Canada should contact their financial advisor to determine whether securities of the Ninepoint Partners LP Funds referred to on this website may be lawfully sold in their jurisdiction. Certain statements in this website are “forward-looking statements” which reflect Ninepoint Partners LP’s expectations regarding future growth, supply and demand of assets, any appreciation in the value of assets, results of operations, performance and business prospects and opportunities. Wherever possible, words such as “may”, “would”, “could”, “will”, “anticipate”, “believe”, “plan”, “expect”, “intend”, “estimate”, “aim”, “endeavour” and similar expressions have been used to identify these forward-looking statements. Such forward-looking statements reflect Ninepoint Partners LP’s current beliefs with respect to future events and are based on information currently available to Ninepoint Partners LP. Forward-looking statements involve significant known and unknown risks, uncertainties and assumptions. A number of factors could cause actual results, performance or achievements to be materially different from any future results, performance or achievements that may be expressed or implied by such forward-looking statements including, without limitation, those risks and uncertainties discussed elsewhere on this website. Should one or more of these risks or uncertainties materialize, or should assumptions underlying the forward-looking statements prove incorrect, actual results, performance or achievements could vary materially from those expressed or implied by the forward-looking statements contained in this website. These factors should be considered carefully and prospective investors should not place undue reliance on these forward-looking statements. Although the forward looking statements contained on this website are based upon what Ninepoint Partners LP currently believes to be reasonable assumptions, Ninepoint Partners LP cannot assure prospective investors that actual results, performance or achievements will be consistent with these forward-looking statements. These forward-looking statements are made as of the date of inclusion on this website, and Ninepoint Partners LP does not intend, and Ninepoint Partners LP does not assume any obligation, to update or revise these forward-looking statements to reflect new events or circumstances.